Answered step by step

Verified Expert Solution

Question

1 Approved Answer

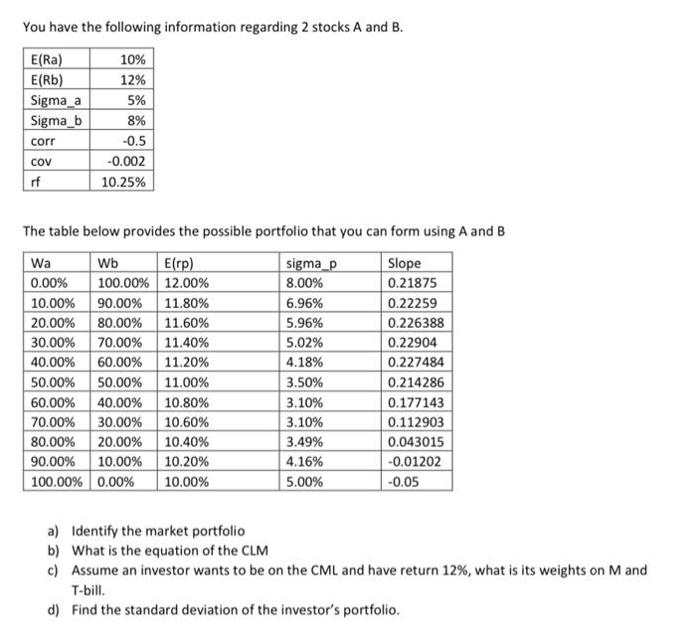

You have the following information regarding 2 stocks A and B. E(Ra) 10% E(Rb) 12% Sigma_a 5% Sigma_b 8% corr -0.5 COV -0.002 rf

You have the following information regarding 2 stocks A and B. E(Ra) 10% E(Rb) 12% Sigma_a 5% Sigma_b 8% corr -0.5 COV -0.002 rf 10.25% The table below provides the possible portfolio that you can form using A and B Wa Wb 0.00% 100.00% E(rp) 12.00% sigma_p Slope 8.00% 0.21875 10.00% 90.00% 11.80% 6.96% 0.22259 20.00% 80.00% 11.60% 5.96% 0.226388 30.00% 70.00% 11.40% 5.02% 0.22904 40.00% 60.00% 11.20% 4.18% 0.227484 50.00% 50.00% 11.00% 3.50% 0.214286 60.00% 40.00% 10.80% 3.10% 0.177143 70.00% 30.00% 10.60% 3.10% 0.112903 80.00% 20.00% 10.40% 3.49% 0.043015 90.00% 10.00% 10.20% 4.16% -0.01202 100.00% 0.00% 10.00% 5.00% -0.05 a) Identify the market portfolio b) What is the equation of the CLM c) Assume an investor wants to be on the CML and have return 12%, what is its weights on M and T-bill. d) Find the standard deviation of the investor's portfolio.

Step by Step Solution

★★★★★

3.50 Rating (157 Votes )

There are 3 Steps involved in it

Step: 1

SOLUTION a The market portfolio is the portfolio that has the expected return of the ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516