you need to pick two options. One Put and one call. You will need to fill out all the information on this spread sheet

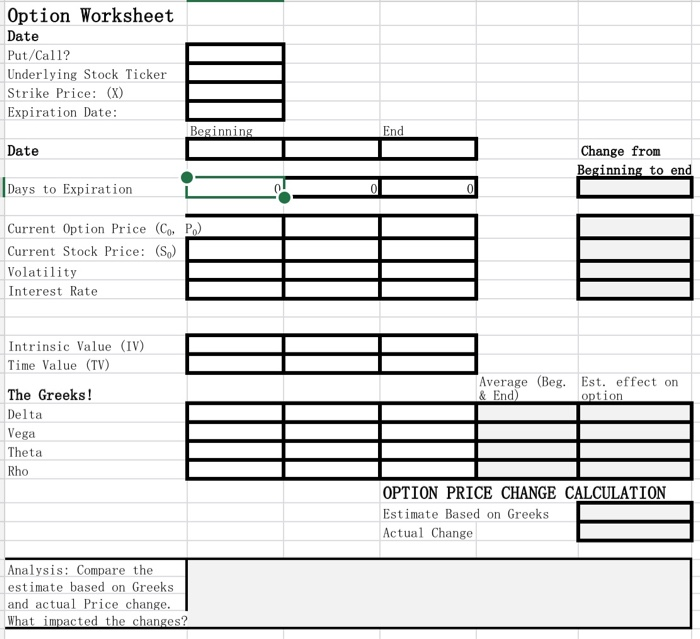

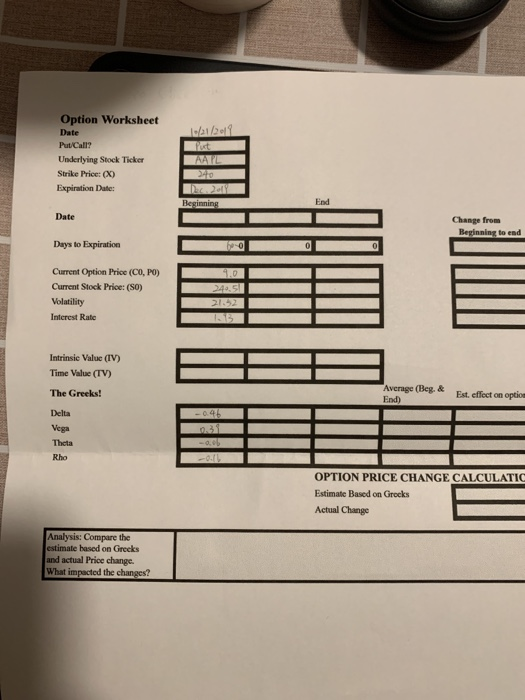

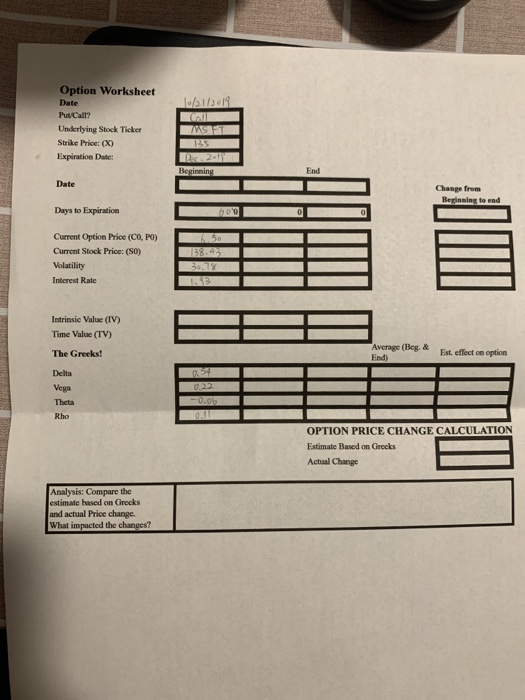

Option Worksheet Date Put/Call? Underlying Stock Ticker Strike Price: (X) Expiration Date: Beginning End Date Change from Beginning to end Days to Expiration ( 0 0 Current Option Price Co, P.) Current Stock Price: (S.) Volatility Interest Rate Intrinsic Value (IV) Time Value (TV) Average (Beg. Est. effect on & End) option The Greeks! Delta Vega Theta Rho OPTION PRICE CHANGE CALCULATION Estimate Based on Greeks Actual Change Analysis: Compare the estimate based on Greeks and actual Price change. What impacted the changes? Option Worksheet Date 10/21/2017 Put/Call? Underlying Stock Ticker Strike Price: (X) Expiration Date: AAL 240 Beginning End Date Change from Beginning to end Days to Expiration 4.0 24,51 Current Option Price (CO, PO) Current Stock Price: (SO) Volatility Interest Rate 1.13 Intrinsic Value (IV) Time Value (TV) The Greeks! Average (Beg. & Est. effect End) option -0.46 Delta Vega Theta Rho OPTION PRICE CHANGE CALCULATIC Estimate Based on Grocks Actual Change Analysis: Compare the estimate based on Greeks and actual Price change. What impacted the changes? Option Worksheet Date 1/21/2018 Put/Call? Underlying Stock Ticker Strike Price: (X) Expiration Date: Beginning Date Change from Beginning to end Days to Expiration hoo 6.50 Current Option Price (CO, PO) Current Stock Price: (SO) Volatility Interest Rate 1.93 Intrinsic Value (IV) Time Value (TV) The Greeks! Average (Beg. & Erd) Est effect option Delta Vega Theta -0.01 0. Rho OPTION PRICE CHANGE CALCULATION Estimate Based on Greeks Actual Change Analysis: Compare the estimate based on Grecks and actual Price change. What impacted the changes? Option Worksheet Date Put/Call? Underlying Stock Ticker Strike Price: (X) Expiration Date: Beginning End Date Change from Beginning to end Days to Expiration ( 0 0 Current Option Price Co, P.) Current Stock Price: (S.) Volatility Interest Rate Intrinsic Value (IV) Time Value (TV) Average (Beg. Est. effect on & End) option The Greeks! Delta Vega Theta Rho OPTION PRICE CHANGE CALCULATION Estimate Based on Greeks Actual Change Analysis: Compare the estimate based on Greeks and actual Price change. What impacted the changes? Option Worksheet Date 10/21/2017 Put/Call? Underlying Stock Ticker Strike Price: (X) Expiration Date: AAL 240 Beginning End Date Change from Beginning to end Days to Expiration 4.0 24,51 Current Option Price (CO, PO) Current Stock Price: (SO) Volatility Interest Rate 1.13 Intrinsic Value (IV) Time Value (TV) The Greeks! Average (Beg. & Est. effect End) option -0.46 Delta Vega Theta Rho OPTION PRICE CHANGE CALCULATIC Estimate Based on Grocks Actual Change Analysis: Compare the estimate based on Greeks and actual Price change. What impacted the changes? Option Worksheet Date 1/21/2018 Put/Call? Underlying Stock Ticker Strike Price: (X) Expiration Date: Beginning Date Change from Beginning to end Days to Expiration hoo 6.50 Current Option Price (CO, PO) Current Stock Price: (SO) Volatility Interest Rate 1.93 Intrinsic Value (IV) Time Value (TV) The Greeks! Average (Beg. & Erd) Est effect option Delta Vega Theta -0.01 0. Rho OPTION PRICE CHANGE CALCULATION Estimate Based on Greeks Actual Change Analysis: Compare the estimate based on Grecks and actual Price change. What impacted the changes