Answered step by step

Verified Expert Solution

Question

1 Approved Answer

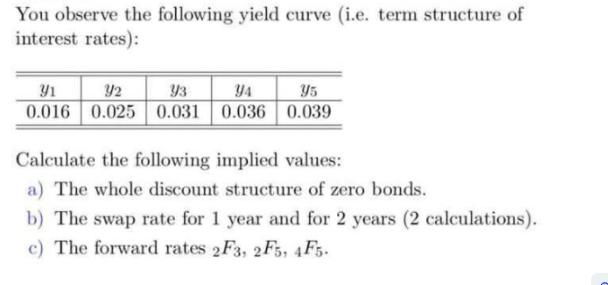

You observe the following yield curve (i.e. term structure of interest rates): 9/1 Y2 Y3 YA Y5 0.016 0.025 0.031 0.036 0.039 Calculate the

You observe the following yield curve (i.e. term structure of interest rates): 9/1 Y2 Y3 YA Y5 0.016 0.025 0.031 0.036 0.039 Calculate the following implied values: a) The whole discount structure of zero bonds. b) The swap rate for 1 year and for 2 years (2 calculations). c) The forward rates 2F3, 2F5, 4F5.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

a The whole discount structure of zero bonds can be calculated as follows The discount factor for ye...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Management

Authors: Eugene F. Brigham, Joel F. Houston

14th edition

1285867971, 978-1305480742, 1305480740, 978-0357686393, 978-1285867977