Answered step by step

Verified Expert Solution

Question

1 Approved Answer

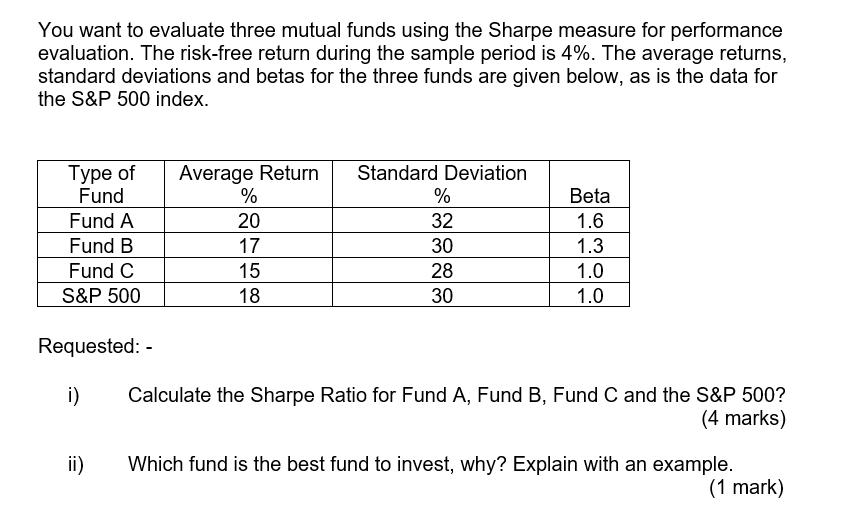

You want to evaluate three mutual funds using the Sharpe measure for performance evaluation. The risk-free return during the sample period is 4%. The

You want to evaluate three mutual funds using the Sharpe measure for performance evaluation. The risk-free return during the sample period is 4%. The average returns, standard deviations and betas for the three funds are given below, as is the data for the S&P 500 index. Type of Fund Average Return Standard Deviation % % Beta Fund A 20 32 1.6 Fund B 17 30 1.3 Fund C 15 28 1.0 S&P 500 18 30 1.0 Requested: - i) Calculate the Sharpe Ratio for Fund A, Fund B, Fund C and the S&P 500? (4 marks) ii) Which fund is the best fund to invest, why? Explain with an example. (1 mark)

Step by Step Solution

★★★★★

3.38 Rating (148 Votes )

There are 3 Steps involved in it

Step: 1

i To calculate the Sharpe Ratio for each fund and the SP 500 index we use the formula Sharpe Ratio Average Return RiskFree Rate Standard Deviation a For Fund A Sharpe Ratio A ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe

10th edition

978-0077511388, 78034779, 9780077511340, 77511387, 9780078034770, 77511344, 978-0077861759