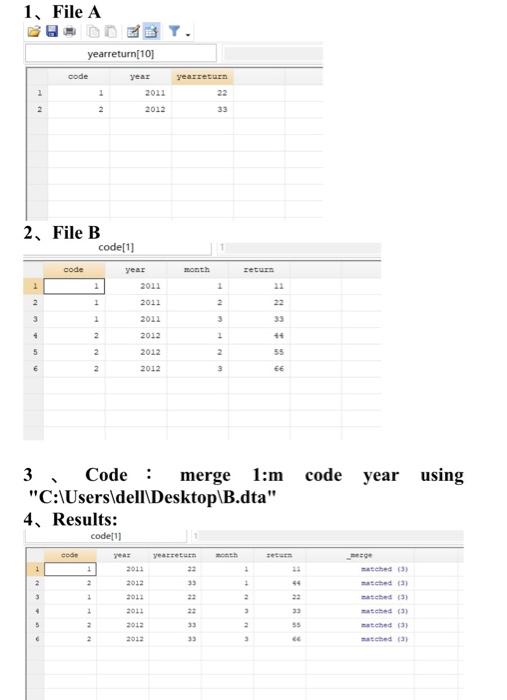

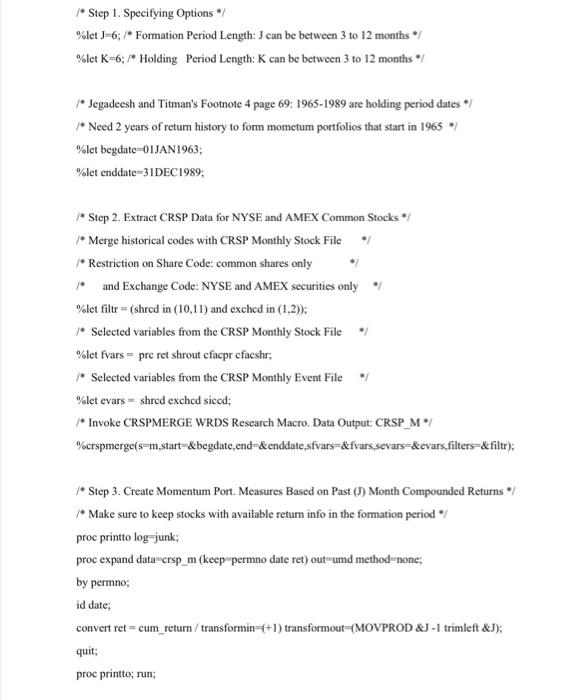

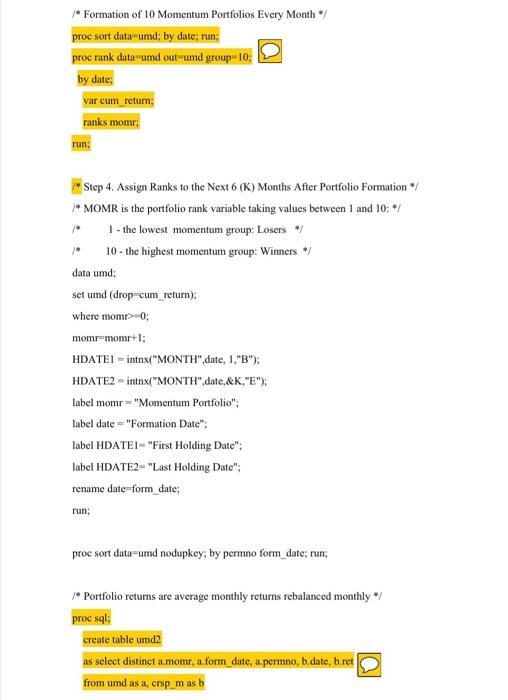

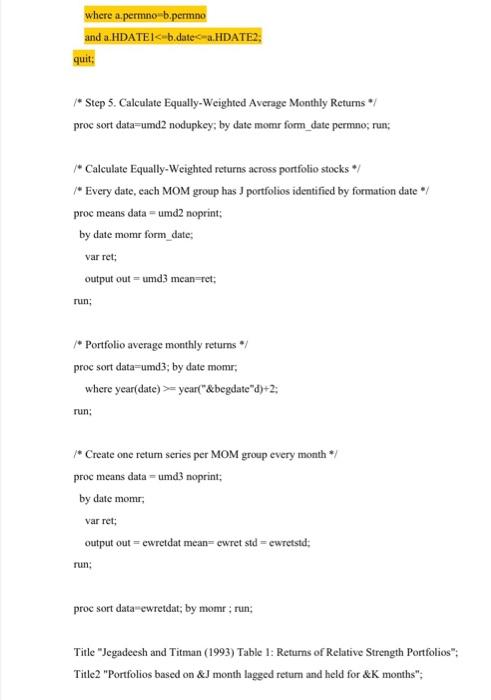

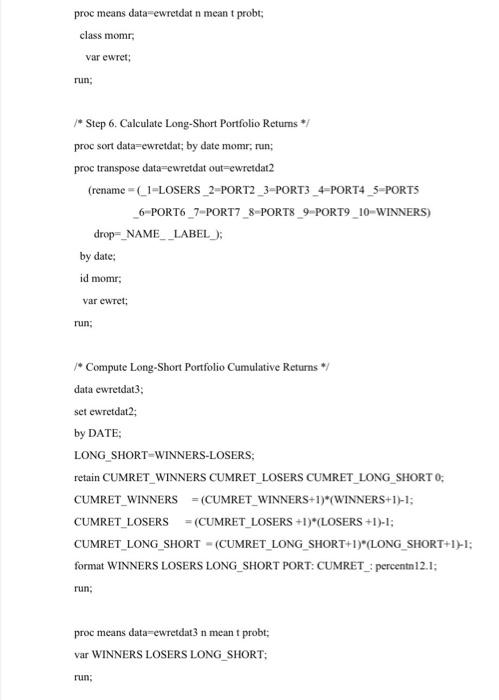

You will present your trading strategy. Specifically, you are expected to include following points: 1. Motivation: the economic intuition why you chose that indicator to construct trading strategy 2. Show the main steps of how you construct your trading strategy, including data selection, sample period, the main sorting variable, the sorting process and models you are going to use to calculate abnormal returns (such as Fama and French 3 factor or 5 factor models). 3. Report the average monthly raw returns of each portfolio (might be terciles, quintiles or other portfolios depending on your setting) and the H-L portfolio (or might be L-H). 4. Report the average monthly abnormal returns of each portfolio and H-L portfolio with t-statistics. 5. Further analysis will be appreciated but not mandatory. On your presentation day, please also send me your printed report. Your report needs to incorporate the contents you present, and your also need to show the following parts: 1. The main programming for your analysis. 2. The detailed contribution of each group member, especially, who is responsible for the programming, and weighted contribution of each member to indicate whether you think your group members are equally contributed to the project. 1. File A Code yearreturn[10] year 1 2011 2012 yearreturn 22 2 T 2 33 2. File B code(1) code return 2 3 year 2011 2011 2012 2012 2012 2012 2 2 3 4 + 1 T 5 2 55 2 3 EE year using 3 Code: merge 1:m code "C:\Users\dell\Desktop\B.dta" 4. Results: codeu code yeatreturn moth 1 1 + watched 3) sched 2 44 2 1 2012 2012 2011 2012 3 33 22 23 33 4 c 23 watched (5) watched (3) watched watched 9 2 2012 35 2012 3 C /* Step 1. Specifying Options %let J-6; /* Formation Period Length: I can be between 3 to 12 months */ %let K-6; Holding Period Length: K can be between 3 to 12 months * Jegadeesh and Titman's Footnote 4 page 69: 1965-1989 are holding period dates * * Need 2 years of return history to form mometum portfolios that start in 1965 %let begdate-OLJAN1963: %let enddate=31DEC1989; * Step 2. Extract CRSP Data for NYSE and AMEX Common Stocks *Merge historical codes with CRSP Monthly Stock File * Restriction on Share Code: common shares only * and Exchange Code: NYSE and AMEX securities only %let filtr = (shred in (10,11) and exched in (1.2)): * Selected variables from the CRSP Monthly Stock File / %let fvars = pre ret shrout cfacpr cfacshr; * Selected variables from the CRSP Monthly Event File %let evars- shred exchod sicod: * Invoke CRSPMERGE WRDS Research Macro. Data Output: CRSP_M* %crspmerge(s-m,start-&begdate,end=&enddate sfvars=&fvars,sevars=&evars,filters=&filtr); *Step 3. Create Momentum Port. Measures Based on Past (1) Month Compounded Returns - Make sure to keep stocks with available return info in the formation period proc printto log-junk proc expand data crsp_m (keep permno date ret) outumd method=none; by permno; id date; convert ret = cum_return/transformin=t+1) transformout=(MOVPROD &J-1 trimleft &J). quit: proc printto; run: * Formation of 10 Momentum Portfolios Every Month */ proc sort data-umd; by date; run: proc rank data-umd out umd group 10; by date: var cum_return; ranks mome: hun; / Step 4. Assign Ranks to the Next 6 (K) Months After Portfolio Formation * MOMR is the portfolio rank variable taking values between 1 and 10: */ 1 - the lowest momentum group: Losers * 10- the highest momentum group: Winners data umd set umd (drop-cum_return): where momr0; momr-momr+1; HDATEI - intx("MONTH", dlate,1,"B"); HDATE2 -intnx("MONTH",date,&K,"E"); label momr="Momentum Portfolio": Tabel date="Formation Date": label HDATEI="First Holding Date"; label HDATE2-"Last Holding Date": rename date=form_date; run: proc sort data-umd nodupkey; by permno form_date; run: Portfolio retums are average monthly returns rebalanced monthly proc sql: create table und2 as select distinct a.mom, a.form date, a.permno, b.date, b.ret from umd as a, crsp mas b where a permno b.permno and a.HDATEI