Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Your group has been engaged by MSS Auto Parts Ltd as cost consultants to review the company's present cost accounting procedures. The CEO of

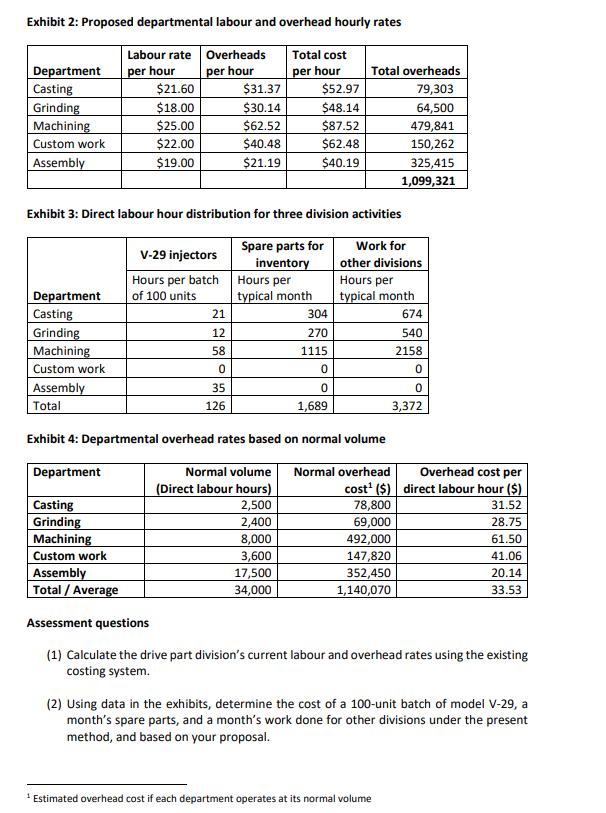

Your group has been engaged by MSS Auto Parts Ltd as cost consultants to review the company's present cost accounting procedures. The CEO of MSS Auto Parts seeks your analysis and recommendations about the accuracy of the current costing system in arriving at the true product costs and its usefulness in providing relevant data to assess managerial performance. MSS Auto Parts Ltd is a relatively small supplier of selected vehicle parts to large automobile manufacturing companies. MSS competed on price with large suppliers that were long established in the market. MSS had competed successfully in the past by focussing on parts that were of small volume (relative to the industry) and hence its competitors could not take advantage of economies of scale. You begin your cost analysis study in the company's drive parts division which accounted for about 40% of the company's sales. This division contained five production departments: Department Casting Grinding Machining Custom work Assembly Focus Production of cases, valves, and other such parts Preparation of parts for further machining Performing machining operations on all standard products Performing operations on custom products. Assembling and testing of all products (both standard and custom) Custom products passed through all five departments while standard products passed through all departments except custom work. Spare parts produced for inventory went through only the first three departments. Both standard and custom products were produced to order. There were no inventories of completed drive parts. Your initial study of the accounting records of the company revealed that except for materials cost, all product costing was done based on a single plat-wide direct labour hour rate. This rate included both direct labour and factory overhead costs. Each batch of products was assigned its labour and overhead cost by having workers charge their time to the job number assigned to the batch and then multiplying the total hours charged to the job number by the hourly rate. Exhibit 1 presents relevant data which can be used to calculate July hourly rates. Based on your study, you contemplate that because the average labour skill level varied from department to department, each department should have its own hourly costing rate. With this approach, time would be charged to each batch by department; then the hours charged by the department would be multiplied by that department's costing rate to arrive at a departmental labour and overhead cost for the batch which would be added to the material cost of the batch to obtain the production cost of the batch. You decided to see what impact this approach would have on product costs. The division's accountant pointed out that labour and payroll costs were already traceable to departments. Also, some overhead items such as departmental supervisors' salaries and equipment depreciation could be charged directly to the relevant department. However, many other overhead items including heating costs, electricity, property taxes, and insurance would need to be allocated to each department if the new approach were implemented. Accordingly, you determined a reasonable allocation basis for each of these costs and then used them to recast July's costs on a departmental basis. You then calculated hourly rates for each department (shown in Exhibit 2). To obtain some numbers to present to the CEO, you decided to apply the proposed approach to three CFI division activities: Production of V-29 fuel injectors (the company's best-selling product), production of spare parts for inventory, and work done by the drive parts division for company's other divisions. Exhibit 3 summarises the hourly requirements of those activities by department. You then costed three activities using both the July plant wide rate and the re-casted July departmental rates (based on the alternative you plan to propose). Upon seeing the numbers, the president noted that there was a substantial difference in the indicated cost of V-29 fuel injectors as calculated under the present and proposed methods. The CEO concluded that the present method was therefore probably leading to incorrect inferences about the profitability of each product. The CEO therefore was leaning towards adopting the new method but told your group that the department supervisors should be consulted before any change was made. Your proposed method prompted strong opposition from some of the supervisors. The supervisors of the outside departments for which the drive parts division did work each month felt it would be unfair to increase their costs by increasing charges from the drive parts division. One of them stated: The drive parts division handles our department's overflow machining work when we are operating at full capacity. I can't control costs in the drive parts division, but if they increase their charges, I'll never be able to meet my department's cost targets. They're already charging us more than what we can do the work for in our own department, if we had enough capacity, and you're proposing to charge us further more! Also opposed was the production manager of the drive parts division: My department supervisors have got enough to do getting good quality output to our customers on time. They don't have time to become bookkeepers. Why do we need this extra complication? The company's sales manager also did not favour the proposal, telling your group: We already have trouble being competitive with the big companies in our industry. If we start playing games with our costing system, then we'll have to start changing our prices. Your group is new here, so perhaps you don't realise that we have to carry sone low-profit or even loss items in order to sell the more profitable ones. As far as I am concerned, if a product line is showing an Page 2 of 5 adequate profit, I'm not hung up about cost variations among the items within the line. The strongest criticism of your group's proposal came from the company's finance director: Departmentalising the costing rate may be a good idea, but I'm not sure you're tackling the main problem. How can these cost estimates be useful if you change the rates every month? When volume is rising all our products make money no matter which system you use. But when overall volume is falling, some products begin to show losses. I don't know if they're really losing money or whether they just can't carry a full share of the cost of idle capacity. I don't see how your system is going to help me answer that question. Faced with all these arguments, your group decided to run some more numbers before going back to the CEO. After seeking estimates of the monthly volume at which each of the five production departments typically operate over the course of the year (normal volume), your group assembled a new set of overhead cost estimates and recalculated the proposed overhead rates, as shown in Exhibit 4. Finally, your group recalculated the labour and overhead costs of a 100 units lot of model V-29 fuel injectors and of a typical month's spare parts production and work for other divisions, based on the "normalised" departmental rates. When you circulated these revised calculations, the production manager of the drive parts division was even more concerned than before: That's even worse! Now you're piling paperwork on paperwork! And on top of everything, we won't be able to charge out all our costs. What am I supposed to do with the costs in machining and assembly if I can't charge them to products or spare parts or the work we do for other divisions? When you reported the various managers' opposition to the CEO, the CEO replied: You're not telling me anything that I haven't already heard from unsolicited phone calls from several supervisors the last few days. I don't want to cram anything down their throats, but I'm still not satisfied our current system is adequate. What do you think we should do? Exhibit 1: Labour cost, labour hours and overheads of the drive parts division Department Labour cost ($) Labour hours 54,604 2,528 38,520 2,140 191,876 7,675 81,664 3,712 291,784 15,357 31,412 Casting Grinding Machining Custom work Assembly Total Overheads 658,448 1,099,321 Exhibit 2: Proposed departmental labour and overhead hourly rates Labour rate Overheads per hour Total cost per hour per hour Department Casting Grinding Machining Custom work Assembly Department Casting Grinding Machining Custom work Assembly Total Department $21.60 $18.00 $25.00 $22.00 $19.00 Casting Grinding Machining Custom work Exhibit 3: Direct labour hour distribution for three division activities Spare parts for inventory Assembly Total / Average V-29 injectors Hours per batch of 100 units 21 12 58 0 $31.37 $30.14 $62.52 $40.48 $21.19 35 126 Hours per typical month $52.97 $48.14 $87.52 $62.48 $40.19 Normal volume (Direct labour hours) 2,500 2,400 8,000 3,600 17,500 34,000 304 270 1115 Exhibit 4: Departmental overhead rates based on normal volume Normal overhead cost ($) 78,800 69,000 492,000 Total overheads 79,303 64,500 479,841 150,262 0 0 1,689 Work for other divisions 325,415 1,099,321 Hours per typical month 147,820 352,450 1,140,070 674 540 2158 0 0 3,372 Estimated overhead cost if each department operates at its normal volume Overhead cost per direct labour hour ($) 31.52 28.75 61.50 41.06 20.14 33.53 Assessment questions (1) Calculate the drive part division's current labour and overhead rates using the existing costing system. (2) Using data in the exhibits, determine the cost of a 100-unit batch of model V-29, a month's spare parts, and a month's work done for other divisions under the present method, and based on your proposal. (3) Are the cost differences among the methods significant? What causes these differences? (4) Assume that producing a batch of 100 of model V-29 injectors requires 126 hours, distributed by department as shown in Exhibit 3, and $4,200 worth of materials. MSS Auto Parts sells these injectors at $113 each. Should the company increase the selling price of V-29? Should V-29 be dropped from the product line? (Answer using both the present method and your first proposed method). (5) Assume that MSS Auto Parts also offers a model V-30 that is identical to V-29 injectors in all important aspects, including price, but is preferred for some applications because of certain design features. Because of the V-30's relatively low sales volume, the company buys certain major components for the V-30 from outside suppliers rather than making them in-house. The total cost of materials and purchased parts for 100 units of model V-30 is $8,000; the labour required per 100 units is 12, 7, 17 and 35 hours respectively in casting, grinding, machining, and assembly departments. If a customer ordered 100 units and said that either model V-29 or V-30 would be acceptable, which model should the company ship? (Answer using only the first proposed costing method and the assumptions regarding V-29 from Question 4). (6) What benefits, if any, do you see to MSS Auto Parts if either proposed costing method is adopted? Consider this question from the standpoint of (a) product pricing, (b) cost control, (c) inventory valuation, (d) charges to outside departments, (e) measuring department's performance. What do you think MSS Auto Parts should do regarding their costing procedures? (0.4+ 1.6+2+ 2.5 +2.5 + 6 = 15 Marks)

Step by Step Solution

★★★★★

3.32 Rating (149 Votes )

There are 3 Steps involved in it

Step: 1

A NSWER 1 Calculation of the current labour and overhead rates using the existing costing system Total labour cost 658448 Total direct labour hours 54604 38520 2528 7675 15357 118684 hours Current pla...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations of Financial Management

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen, Doug Short, Michael Perretta

10th Canadian edition

1259261018, 1259261015, 978-1259024979