Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Your Starting Point: Value Proposition First Meeting - Welcoming Duane and Eric to Your Office Financial Planner: Congratulations to both of you on your

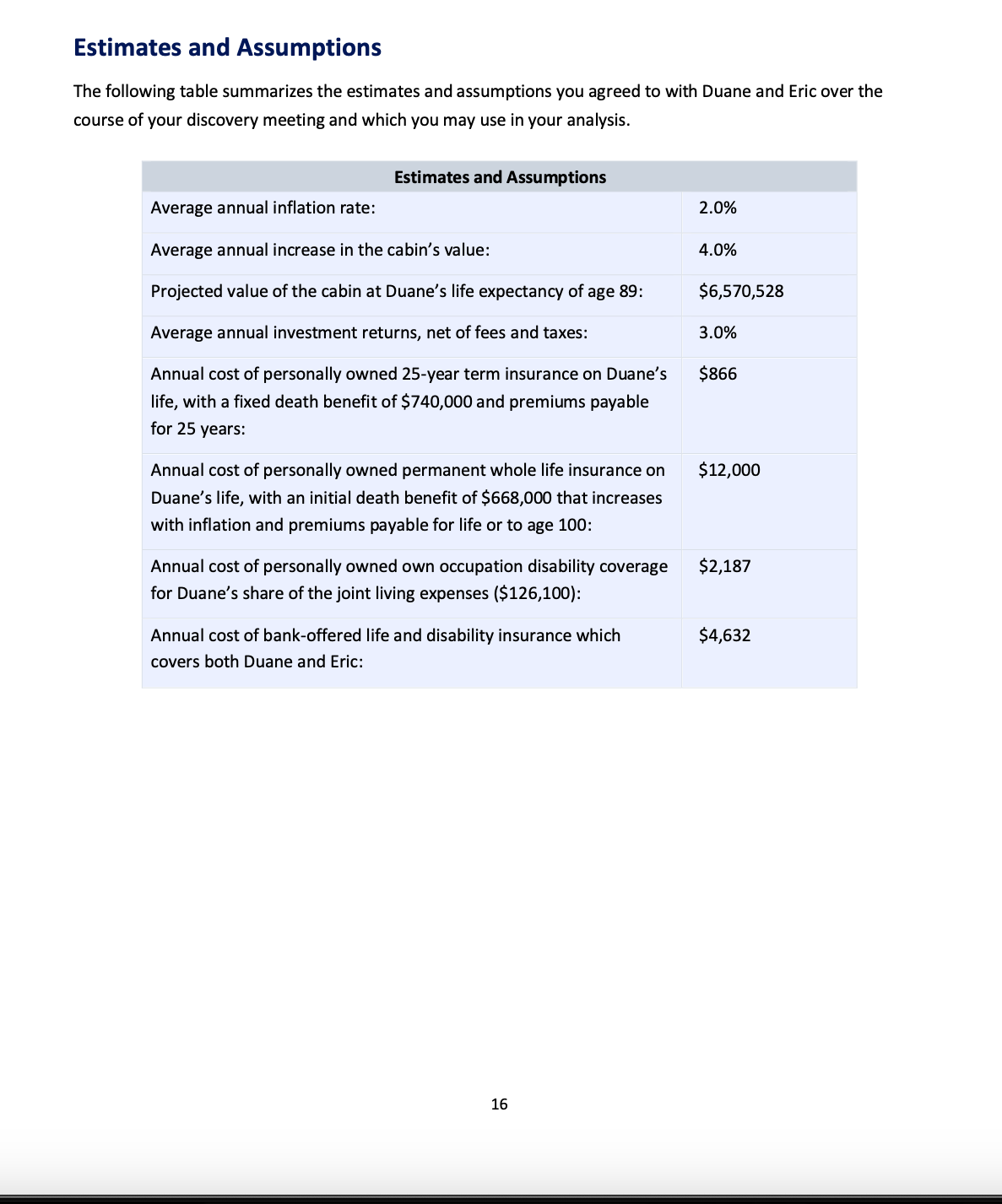

Your Starting Point: Value Proposition First Meeting - Welcoming Duane and Eric to Your Office Financial Planner: Congratulations to both of you on your upcoming wedding! Eric, it's great to meet you at last. How are the wedding plans coming? Eric: We're trying to keep it simple, but there's a lot more to do than I expected. Duane: Yes, it seems every night we're going over our checklists to make sure we haven't forgotten anything. Now I know why people use wedding planners! And we're preparing to move into our new condo at the same time. Financial Planner: I know you withdrew funds for the down payment for the condo. Can you tell me a bit about where you are in the process and how you're feeling about moving into a new place? Eric: Yes, we both can't wait to move in. It's the perfect condo to start our married life in! However, buying the condo is a big financial commitment. One thing we want to talk to you about is how I can afford to stay in the condo should something happen to Duane. Duane's dad died prematurely and his brother was killed in an accident, so you never know. I'm a bit worried because we will have quite a big mortgage, and I don't think I could afford the payments on just my salary. I think I could only take care of the property taxes and other expenses. Financial Planner: It's a great idea to have these conversations now, to deal with any financial concerns before you get married. Did you purchase the condo in joint names? Duane: Yes, it will be Eric's if I die prematurely, and vice versa, but I want to have peace of mind that Eric will be able to afford the mortgage payments if something happens to me and I lose my income. We will both be contributing toward the mortgage and other expenses. When we were pre-approved for a mortgage, our banker mentioned purchasing mortgage insurance, but I'm not sure if it is the best option, based on what I've read. I don't like the idea of paying the same premium for 25 years while the amount of coverage declines. 6 Financial Planner: That's something we can look into and help you make the decision that's the best fit for your situation. While we're on an estate topic, Duane, I know you have a valid will. Do you intend to update it before you get married? Duane: Yes, I do. We both plan to update our wills. Eric and I have talked about our wishes for our estates, and we have appointments set with my lawyer for next month. Eric: Yes, we've had some good conversations. One thing I want to make sure of is that I can leave my estate to the Wild BC organization. Duane and I don't plan to have a family, so helping the environment is my priority. Saving B.C.'s water and forests for future generations is so important to me and I would feel great satisfaction knowing my estate will support that goal. Financial Planner: That's a worthy cause. Have you taken steps to leave your assets to the Wild BC organization? Eric (laughs): Until recently, I haven't really owned much. I do have TFSA and RRSP savings, and I have designated Wild BC as my beneficiary on both. I worry that these savings might be depleted by trying to stay in the condo if something were to happen to Duane. Duane: As you'll remember, my brother didn't leave his family much, so leaving what I can to my nieces is something I want to achieve. I want to have confidence they will be looked after if I die prematurely. But of course, I want to make sure Eric is secure too, being confident that he can stay in the condo. Financial Planner: I see. So, you envision Eric owning the condo-and would your investment assets go to your nieces? Duane: Exactly, and you agree, don't you Eric? Eric: That's right. I totally agree with Duane's thoughts. As I said earlier, I don't think I could afford the mortgage and other payments on just my salary. I fear the thought of having to ask my parents for money-they supported me for a quite a few years. Financial Planner: That makes perfect sense. Duane, do you still have the cabin property your father left you? Duane: Yes. Eric and I are going up there this weekend. Financial Planner: It must be worth substantially more now, being right on the ocean. Prices on the Sunshine Coast have increased significantly recently. Duane: Yes, prices are high. We just did a bit of updating and I think it's probably worth $1 million. My dad paid $22,000 for it originally, and it was worth $90,000 when Jesse and I inherited it twenty years ago. Boy, I have a lot of great memories at that place, hanging out with Eric or having camp weekends with Suzanne and the girls. I look forward to making more memories and I'm happy thinking those I love could have more great days to remember too. Financial Planner: Do you want that property go to your nieces as well? Duane: For sure, yes. I want them to own the cabin eventually. It would be satisfying to know that my father's cabin will stay in the family. That's family property forever. But at the same time, I know how much Eric loves being close to nature and if I were to die in the near future, I want to make sure that he has access to use it whenever he wants, for at least several years after I'm gone. I want the same for Suzanne as well, although as the girls' mother I'm sure she'll always be welcome. Eric: You never know about that. You and your mother don't exactly get along, do you? Duane: Too true, I hadn't thought about that. She hasn't been in my life for so many years. Is it possible to ensure that Suzanne could use the cabin for at least a few years after I'm gone, even if she weren't on the best of terms with my nieces? Financial Planner: We can certainly look at that as part of your plan. Also, there will likely be a tax liability on the cabin property when you die-what about that? Will that come out of your nieces' inheritance? Duane: I hadn't thought about that either. It doesn't seem right that they'd have to pay tax for previous generations, so I'd want to try to avoid that. As much as I can, I want to ensure their inheritance is not depleted by taxes. I guess we have more to work on than I realized. I hope you can help us. Financial Planner: Absolutely, I look forward to it. Second Meeting - Agree on Terms of Engagement At the end of your first meeting, Duane and Eric decided to engage you for financial planning. You explained that you would prepare a Letter of Engagement, a document that describes the planning arrangement and other important aspects of working together. During your meeting with Duane and Eric a week later, you explained each section of the Letter of Engagement, answered their questions and confirmed their understanding of the planning engagement. You reviewed the scope of services you would provide, namely: A written financial plan designed to meet their goals, including recommendations and an implementation plan covering the following areas. . Risk management, including: . Eric's ability to afford mortgage payments if something happened to Duane's income, to ensure he can stay in the condo and that his savings can be left to Wild BC. The potential depletion of Duane's nieces' inheritances resulting from a tax liability on the cabin. Estate planning, including: Duane's wishes for his estate, including his nieces' inheritance and access to the cabin for Eric and sister-in-law Suzanne. You verified that the scope of services sufficiently described what they ultimately expect from you. You reviewed all other clauses and checked for understanding before asking Duane and Eric to sign the letter. Collaborating with Duane and Eric in Advance of the Discovery Meeting: After finalizing the Letter of Engagement, you described the next steps of the planning engagement, specifically, the discovery meeting that will focus on obtaining a deeper understanding of Duane and Eric's financial situation and priorities. You explained to them that, if they provided information in advance of the discovery meeting, you could better prepare by reviewing and making sense of the information. Doing so would allow you to conduct a more efficient meeting by focusing on what their information means instead of starting with basic fact finding. This approach would make the most of your time together which, as busy people, you know they will appreciate. A few days later, you received the following financial information from Duane: Assets TFSA Duane Eric $110,000 $13,200 RRSP $295,000 $26,000 Non-registered investments $945,000 $0 Vehicle (Tesla Model S) $110,000 $0 Sunshine Coast cabin $1,000,000 $0 (ACB $90,000) Liabilities Credit card balance $9,000 $0 Annual Income Salary (gross) Investment income $220,000 $70,000 $37,800 $0 Annual Expenses Lifestyle spending (includes rent) $96,100 $32,100 Income tax $88,600 $13,300 TFSA contributions $6,000 $12,000 RRSP contributions $27,830 $12,600 Non-registered savings $39,270 $0 After receiving the information, and before the discovery meeting, you determined additional quantitative questions you may need to ask. You also prepared a list of personalized qualitative questions taken from the CFP Base Questions for Financial Planning Discovery in the areas of Risk Management and Estate Planning. 11 Third Meeting - Discovery Meeting You begin the discovery meeting by reminding Duane and Eric that it is an opportunity to understand more about their priorities and current situation. By getting to know them and understanding their circumstances, you'll be able to provide meaningful recommendations. You then move to asking your prepared qualitative questions about their family, to engage them and encourage conversation by focusing on a topic that is easy for them to talk about. As the meeting progresses, you uncover the following information. Family Duane and Eric met in Kamloops, British Columbia. Eric lived there at the time and Duane was on a ski holiday. Eric received financial support from his parents until he moved in with Duane. His parents are excited about their wedding and are very proud of Eric for pursuing a career that he is passionate about and becoming financially independent. He is grateful for their support in the hard times and is determined not to disappoint them. Duane (and his brother Jesse) was raised by his father as his mother left the family when Duane was five years old. He has not had contact with her for years but has been told she is in poor health. Duane is very involved in the lives of his nieces Jennifer (age 16) and Jessica (age 14). He gets along well with their mother, Suzanne. Duane and Eric do not plan to have a family. 12 Financial Details Since moving in together, Duane and Eric have shared living expenses in proportion to their incomes. Since Duane earns more, he pays more of the living expenses. This arrangement has allowed Eric to save a substantial portion of his salary. Eric maximizes his RRSP contributions and contributes any surplus cash flow to his TFSA account. Their new condo cost $1,200,000 and required a down payment of $240,000, which was taken from Duane's own non-registered funds. Duane and Eric have been pre-approved by their bank for a mortgage of $960,000, with an interest rate resulting in monthly payments of $4,182, based on a 25-year amortization. Duane estimates their total housing expenses after purchasing the condo will increase by $2,500 per month ($30,000 year). He suggests the difference could be funded by reducing the amount he adds each year to his non-registered investments. The cabin on the Sunshine Coast has an estimated market value of $1,000,000. It required a capital investment for repairs of $10,000, which were recently completed. The cost of repairs would be added to the ACB of $90,000 (the value at the time Duane and Jesse acquired the property). The capital gain if Duane were to die today would therefore be $900,000, resulting in a tax bill of $240,750 based on the highest marginal tax rate in B.C. of 53.5%. It's expected the cabin will continue to appreciate at 4% per year. Risk Management If Duane were unable to work due to a disability, he'd like to be able to maintain his contribution toward their combined expenses. Duane would like the mortgage to be paid off entirely if he were to die prematurely. Duane is confident he could handle the expenses of their condo, including the mortgage payments, if Eric were to die prematurely or become disabled and unable to work. Duane has group life insurance coverage through his employer which has a death benefit equal to his annual salary of $220,000. He recently changed the beneficiary of this insurance to be Eric. With an expected mortgage of $960,000 and group life insurance coverage of $220,000, there would be $740,000 of the mortgage uninsured. Disability Insurance Duane's employer group benefits include mandatory disability insurance with "any occupation" coverage. The benefit would pay 40% of his salary monthly for up to two years in the event of total disability. The benefit is paid in cash and can be directed towards any expense. The benefits would stop if he were able to perform any type of full-time work. Duane pays the premiums via payroll deduction, so any benefits would be tax-free. Eric does not have any life or disability insurance, personally or through his employer. They have been offered mortgage insurance with coverage as follows: Mortgage Insurance Offer A premium of $269 per month for life insurance only, that covers both Duane and Eric; or A premium of $386 per month for life and disability insurance that covers both Duane and Eric. In the event of death, the life insurance proceeds would pay any outstanding mortgage balance. In the event of the inability to work due to disability, the monthly mortgage payments would be paid by insurance benefits for the duration of the disability. The life and disability benefits under the mortgage insurance can only be used towards mortgage liabilities and is not available for other household expenses. Both Duane and Eric are healthy and insurable at standard non-smoking rates. They have ample home and auto insurance coverage. Estate Planning Eric Duane and Eric have an appointment with Duane's lawyer in one month to update their estate documents. They hope to include any relevant strategies that may come from your risk management and estate-related recommendations. The couple also intends to complete prenuptial agreements at the same time they execute their estate documents in case of a breakdown in their relationship. The condo will be purchased in joint names with rights of survivorship and will go to the survivor if one dies. Eric has designated the Wild BC organization as the beneficiary of his RRSP and TFSA. Eric wants his entire estate to go to Wild BC. He is confident that Duane would be in a stable financial position without any inheritance from him and Duane agrees. Eric intends to appoint Duane to be his executor, attorney and health care representative with his sister Julia named as an alternate. Duane Duane's RRSP and TFSA savings name his estate as beneficiary. He recently changed the beneficiary on his group life insurance to be Eric. Duane wants to be sure Eric is financially able to continue living in the condo if he wishes to do so. He feels that if the mortgage was paid, Eric could realize a financial benefit if he chose to sell the property should the property taxes, condo fees and expenses become unaffordable for him. Duane wants Eric to be able to spend time at the cabin for at least several years if Duane were to pass away in the near future. Except for the condo, Duane wants his estate, including the cabin, to go to his nieces. Duane prefers that his niece's inheritance will not be depleted by taxes. Duane intends to appoint his sister-in-law Suzanne as executor and as trustee if her children are still minors at the time of his death, with Eric named as an alternate. He wants Eric to be his attorney and health care representative, with Suzanne named as an alternate. Duane also wants to make sure that Suzanne has access to use the cabin for at least several years if he should die in the near future, even if she isn't on the best of terms with her daughters. Duane is unsure at what ages his nieces will be mature enough to fully receive their inheritances. Similar to Power of Attorney for Personal Care in Ontario and other provinces. 15 Estimates and Assumptions The following table summarizes the estimates and assumptions you agreed to with Duane and Eric over the course of your discovery meeting and which you may use in your analysis. Estimates and Assumptions Average annual inflation rate: 2.0% 4.0% Average annual increase in the cabin's value: Projected value of the cabin at Duane's life expectancy of age 89: Average annual investment returns, net of fees and taxes: $6,570,528 3.0% $866 Annual cost of personally owned 25-year term insurance on Duane's life, with a fixed death benefit of $740,000 and premiums payable for 25 years: Annual cost of personally owned permanent whole life insurance on Duane's life, with an initial death benefit of $668,000 that increases with inflation and premiums payable for life or to age 100: $12,000 Annual cost of personally owned own occupation disability coverage for Duane's share of the joint living expenses ($126,100): $2,187 Annual cost of bank-offered life and disability insurance which covers both Duane and Eric: $4,632 16 46

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Venture capital and the finance of innovation

Authors: Andrew Metrick

2nd Edition

9781118137888, 470454709, 1118137884, 978-0470454701