Answered step by step

Verified Expert Solution

Question

1 Approved Answer

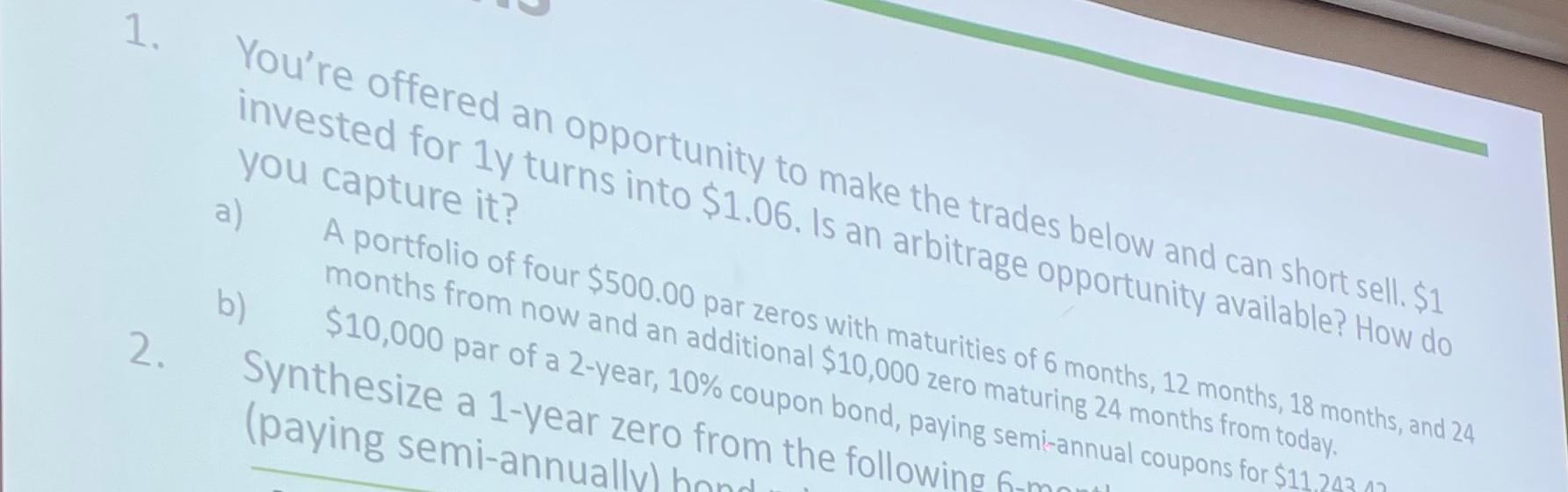

You're offered an opportunity to make the trades below and can short sell. $1 invested for 1y turns into $1.06. Is an arbitrage opportunity available?

You're offered an opportunity to make the trades below and can short sell. $1 invested for 1y turns into $1.06. Is an arbitrage opportunity available? How do you capture it?\ a) A portfolio of four

$500.00par zeros with maturities of 6 months, 12 months, 18 months, and 24 2. Synt

$10,000par of a 2-year,

10%coupon bonic, zero maturing 24 months from today.\ Synthesize a 1-year zero from the following semi-annual coupons for

$11,202.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started