Obtain the S&P 500 Index daily closes for the period from January 1987 to December 2017 and

Question:

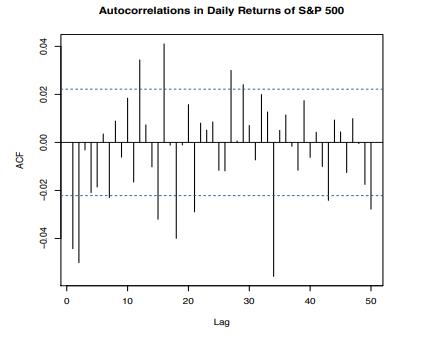

Obtain the S\&P 500 Index daily closes for the period from January 1987 to December 2017 and compute the log returns. These are the data shown in Figure 1.30. Fit an MA(2) model to the returns. Comment on the fit and this method of analysis generally. Can ARMA models add meaningful insight into stock returns?

Figure 1.30:

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Ayush Jain

Subjects in which i am expert:

Computer Science :All subjects (Eg. Networking,Database ,Operating System,Information Security,)

Programming : C. C++, Python, Java, Machine Learning,Php

Android App Development, Xamarin, VS app development

Essay Writing

Research Paper

History, Management Subjects

Mathematics :Till Graduate Level

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: