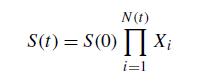

Let S(t) denote the price of a security at time t . A popular model for the

Question:

Let S(t) denote the price of a security at time t . A popular model for the process

{S(t), t ≥ 0} supposes that the price remains unchanged until a “shock”

occurs, at which time the price is multiplied by a random factor. If we let N(t)

denote the number of shocks by time t , and let Xi denote the ith multiplicative factor, then this model supposes that

where $N(t)

i=1 Xi is equal to 1 when N(t) = 0. Suppose that the Xi are independent exponential random variables with rate μ; that {N(t), t ≥ 0} is a Poisson process with rate λ; that {N(t), t ≥ 0} is independent of the Xi ; and that S(0) = s.

(a) Find E[S(t)].

(b) Find E[S2(t)].

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Ashish Bhalla

I have 12 years work experience as Professor for Accounting, Finance and Business related subjects also working as Online Tutor from last 8 years with highly decentralized organizations. I had obtained a B.Com, M.Com, MBA (Finance & Marketing). My research interest areas are Banking Problem & Investment Management. I am highly articulate and effective communicator with excellent team-building and interpersonal skills; work well with individuals at all levels.

17+ Reviews

46+ Question Solved

Related Book For

Question Posted: