The law firm of Spade & Associates hired Dylan Sayers to review the audit of the 2014

Question:

The law firm of Spade & Associates hired Dylan Sayers to review the audit of the 2014 financial statements that Hammer & Wimsey, CPAs, had completed for Golden Sound and Records Company. Specifically, the attorneys engaged Sayers to determine whether the audit of Golden Sound’s inventory of sound equipment and CDs conformed to generally accepted auditing standards. After Golden Sound declared bankruptcy three months ago (eight months after the 2014 audited financial statements were issued), stockholders sued Golden Sound, alleging distribution of misleading financial statements, and Hammer & Wimsey hired Spade & Associates to pre-pare a defense in the event that Hammer & Wimsey were included later in the lawsuit. The first time Golden Sound had been audited was 2014.

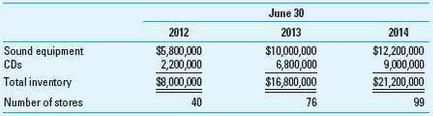

Golden Sound’s business had grown rapidly. The company had 40 stores in 2012, opened 36 more in 2013, and added 23 more (for a total of 99) during 2014. The following accounting information showed the growth of the inventory:

Sayers reviewed the Hammer & Wimsey audit documentation and prepared this summary: In April 2014, Bobby Earl (Hammer & Wimsey audit manager on the Golden Sound engagement) met with Golden Sound’s managers and discussed the procedures for taking the physical inventory as of June 30. Mikki LaTouche (Golden Sound’s chief financial officer) suggested that the auditors’ inventory observation be conducted at the stores located in large cities where Golden Sound had started business. According to LaTouche, “These stores are well stocked with a representative selection of all types of equipment and musical releases available across all the stores. The store managers are well acquainted with the inventory and can conduct an accurate counting with experienced store employees. The newer stores carry less stock, and the managers are relatively new to their jobs. You’ll get a more accurate inventory- taking observation in the more established stores.”

Earl agreed and noted in the audit documentation that the prospect of sending audit teams to distant stores in the Midwestern and Southeastern states (where Golden Sound had established new stores in the past year or so) would be very costly in terms of auditors’ time and travel expenses. Together, LaTouche and Earl selected eight of the stores in the Western Region. Earl supervised experienced audit teams as they observed the inventory counts at these eight stores. The auditors observed that the Golden Sound store managers gave good instructions to the inventory takers and that the count records were in good order. Test counts showed only minor mistakes, which the managers promptly and conscientiously corrected.

Everyone was interested in making accurate counts because Golden Sound had no reliable perpetual inventory records, and the financial statement amounts for inventory were determined by this physical inventory. In fact, Earl wrote in the internal control communication to the board of directors and in the management letter addressed to the CFO the observation that Golden Sound needed to establish reliable inventory records for physical control and profit enhancement. The auditors determined the following inventory amounts in the eight stores. Using the total inventory of $ 1,712,700 in these stores, Earl divided by eight to find the average per store, then multiplied by 99, and projected the total inventory in the amount of $ 21,194,663. Because this amount was only $ 5,337 less than the recorded value of inventory in the general ledger, Earl and the reviewing partner did not perform further work and incorporated the recorded inventory amount of $ 21,200,000 in the 2014 financial statements along with a standard unmodified auditor’s report. Required: Complete Sayers’s engagement by evaluating the Hammer & Wimsey conduct of the inventory portion of the Golden Sound 2014 audit. Use auditor’s responsibilities from Chapter 2 to guide your answer.

Financial StatementsFinancial statements are the standardized formats to present the financial information related to a business or an organization for its users. Financial statements contain the historical information as well as current period’s financial... Distribution

The word "distribution" has several meanings in the financial world, most of them pertaining to the payment of assets from a fund, account, or individual security to an investor or beneficiary. Retirement account distributions are among the most...

Step by Step Answer:

Hammer Wimsey in the persons of Bobby Earl and the unnamed reviewing partner will have a difficult time establishing a defense in terms of claiming to ...View the full answer

Auditing and Assurance Services

ISBN: 978-0077862343

6th edition

Authors: Timothy Louwers, Robert Ramsay, David Sinason, Jerry Straws