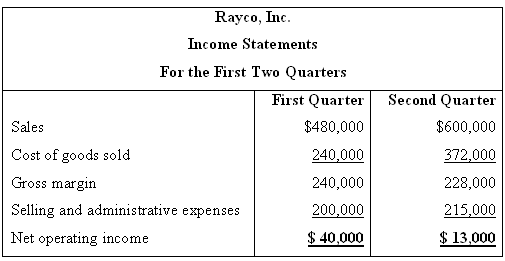

These statements cant be right, said Ben Yoder, president of Rayco, Inc. Our sales in the second

Question:

These statements can’t be right, said Ben Yoder, president of Rayco, Inc. “Our sales in the second quarter were up by 25% over the first quarter, yet these income statements show a precipitous drop in net operating income for the second quarter. Those accounting people have fouled something up.” Mr. Yoder was referring to the following statements (absorption costing basis):

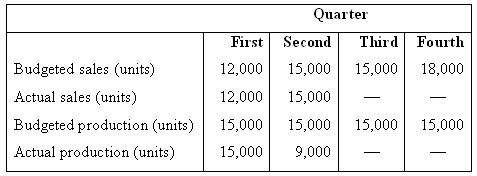

After studying the statements briefly, Mr. Yoder called in the controller to see if the mistake in the second quarter could be located before the figures were released to the press. The controller stated, “I’m sorry to say that those figures are correct, Ben. I agree that sales went up during the second quarter, but the problem is in production. You see, we budgeted to produce 15,000 units each quarter, but a strike on the west coast among some of our suppliers forced us to cut production in the second quarter back to only 9,000 units. That’s what caused the drop in net operating income.” Mr. Yoder was confused by the controller’s explanation. He replied, “This doesn’t make sense. I ask you to explain why net operating income dropped when sales went up and you talk about production! So what if we had to cut back production? We still were able to increase sales by 25%. If sales go up, then net operating income should go up. If your statements can’t show a simple thing like that, then it’s time for some changes in your department!” Budgeted production and sales for the year, along with actual production and sales for the first two quarters, are given below:

The company’s plant is heavily automated, and fixed manufacturing overhead amounts to $180,000 each quarter. Variable manufacturing costs are $8 per unit. The fixed manufacturing overhead is applied to units of product at a rate of $12 per unit (based on the budgeted production shown on the prior page). Any underapplied or overapplied overhead is closed directly to cost of goods sold for the quarter. The company had 4,000 units in inventory to start the first quarter and uses the FIFO inventory flow assumption. Variable selling and administrative expenses are $5 per unit.

Required:

1. What characteristic of absorption costing caused the drop in net operating income for the second quarter and what could the controller have said to explain the problem?

2. Prepare a contribution format variable costing income statement for each quarter.

3. Reconcile the absorption costing and the variable costing net operating income figures for each quarter.

4. Identify and discuss the advantages and disadvantages of using the variable costing method for internal reporting purposes.

5. Assume that the company had introduced Lean Production at the beginning of the second quarter, resulting in zero ending inventory. (Sales and production during the first quarter remain the same.)

a. How many units would have been produced during the second quarter under Lean Production?

b. Starting with the third quarter, would you expect any difference between the net operating income reported under absorption costing and under variable costing? Explain why there would or would not be any difference.

Ending InventoryThe ending inventory is the amount of inventory that a business is required to present on its balance sheet. It can be calculated using the ending inventory formula Ending Inventory Formula =...

Step by Step Answer:

1 Under absorption costing net operating income depends on both production and sales For this reason the controllers explanation was accurate He should have pointed out however that the reduction in p...View the full answer

Managerial Accounting

ISBN: 978-0697789938

13th Edition

Authors: Ray H. Garrison, Eric W. Noreen, Peter C. Brewer