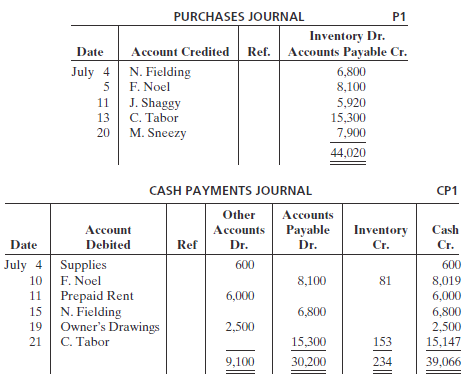

Presented below and on page 348 are the purchases and cash payments journals for Richmond Co. for

Question:

Presented below and on page 348 are the purchases and cash payments journals for Richmond Co. for its first month of operations.

In addition, the following transactions have not been journalized for July. The cost of all merchandise sold was 65% of the sales price.July 1 The founder, N. Richmond, invests $80,000 in cash.6 Sell merchandise on account to Abi Co. $6,200 terms 1/10, n/30.7 Make cash sales totaling $6,000.8 Sell merchandise on account to S. Beauty $3,600, terms 1/10, n/30.10 Sell merchandise on account to W. Pitts $4,900, terms 1/10, n/30.13 Receive payment in full from S. Beauty.16 Receive payment in full from W. Pitts.20 Receive payment in full from Abi Co.21 Sell merchandise on account to H. Prince $5,000, terms 1/10, n/30.29 Returned damaged goods to N. Fielding and received cash refund of $420.Instructions(a) Open the following accounts in the general ledger.101 Cash112 Accounts Receivable120 Inventory127 Supplies131 Prepaid Rent201 Accounts Payable301 Owner??s Capital306 Owner??s Drawings401 Sales Revenue414 Sales Discounts505 Cost of Goods Sold631 Supplies Expense729 Rent Expense(b) Journalize the transactions that have not been journalized in the sales journal, the cash receipts journal (see Illustration 7-9), and the general journal.(c) Post to the accounts receivable and accounts payable subsidiary ledgers. Follow the sequence of transactions as shown in the problem.(d) Post the individual entries and totals to the general ledger.(e) Prepare a trial balance at July 31, 2012.(f) Determine whether the subsidiary ledgers agree with the control accounts in the general ledger.(g) The following adjustments at the end of July are necessary.(1) A count of supplies indicates that $140 is still on hand.(2) Recognize rent expense for July, $500.Prepare the necessary entries in the general journal. Post the entries to the general ledger.(h) Prepare an adjusted trial balance at July 31,2012.

Accounts ReceivableAccounts receivables are debts owed to your company, usually from sales on credit. Accounts receivable is business asset, the sum of the money owed to you by customers who haven’t paid.The standard procedure in business-to-business sales is that...

Step by Step Answer:

a d g b c Accounts Receivable Subsidiary Ledger e f g h Cash Date ...View the full answer

Accounting Principles

ISBN: 978-0470534793

10th Edition

Authors: Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso