Exercise 7.7 Consider the random variable where Z1, Z2, . . . are independent and identically distributed

Question:

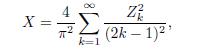

Exercise 7.7 Consider the random variable

where Z1, Z2, . . . are independent and identically distributed standard Gaussian variables. Show that the law of X is infinitely divisible. If Y is a L´evy process with Y (1) = X, find a representation for Y (t), for any t > 0. Does Y have a Brownian component?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Daniel Kimutai

I am a competent academic expert who delivers excellent writing content from various subjects that pertain to academics. It includes Electronics engineering, History, Economics, Government, Management, IT, Religion, English, Psychology, Sociology, among others. By using Grammarly and Turnitin tools, I make sure that the writing content is original and delivered in time. For seven years, I have worked as a freelance writer, and many scholars have achieved their career dreams through my assistance.

1+ Reviews

10+ Question Solved

Related Book For

Statistical Methods For Financial Engineering

ISBN: 9781032477497

1st Edition

Authors: Bruno Remillard

Question Posted: