On 1 January 2008, an entity issued EUR 4m of 7 per cent convertible loan stock. The

Question:

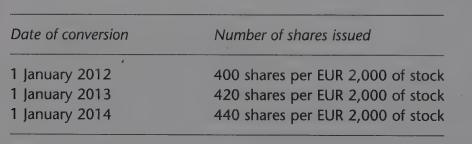

On 1 January 2008, an entity issued EUR 4m of 7 per cent convertible loan stock. The holders of this stock may choose to convert the stock to ordinary shares on 1 January 2012, 2013 or 2014. The number of ordinary shares into which the stock will be converted is as follows:

The entity’s net income for the year ended 30 September 2009 was EUR 4.4m. The comparative figure for the year ended 30 September 2008 was EUR 4.8m. The entity pays tax at 30 per cent. On 1 October 2007, the entity’s issued share capital consisted of 1.5 million 12 per cent preference shares of EUR 2 each and 5 million ordinary shares of EUR 0.40 each.

On 1 April 2009 the entity issued a further 500,000 ordinary shares at market price.

The preference dividend was paid in full in both the year ended 30 September 2008 and the year ended 30 September 2009.

(a) Calculate basic EPS and diluted EPS for the year ended 30 September 2008.

(b) Calculate basic EPS and diluted EPS for the year ended 30 September 2009.

Step by Step Answer:

To calculate the basic and diluted earnings per share EPS for the entity well use the following formulas 1 Basic EPS textBasic EPS fractextNet Income textPreference DividendstextWeighted Average Numbe...View the full answer

Advanced Financial Accounting An International Approach

ISBN: 9780273712749

1st Edition

Authors: Jagdish Kothari, Elisabetta Barone