On 1 January 20x3, P Co acquired 90% of the ownership interest of Y Co for $2,000,000.

Question:

On 1 January 20x3, P Co acquired 90% of the ownership interest of Y Co for $2,000,000. At that date, the following relate to Y Co:

It was estimated that the intellectual property had a remaining useful life of five years from 1 January 20x3. The fair value of non-controlling interests of Y Co as at the date of acquisition was $200,000. There was no change in the share capital of Y Co since acquisition date. There were no other items in equity other than share capital and retained earnings.

On 1 July 20x4, Y Co transferred its equipment to P Co at a transfer price of $120,000. The equipment was purchased from external vendors on 1 July 20x1 at a price of $140,000. Its estimated useful life was five years from the date of purchase and it had no residual value. The original estimates remained unchanged at the date of transfer.

Y Co sold inventory to P Co on the following dates:

Losses on transfers are indicative of impairment loss in the underlying asset. Tax rate was 20%. Tax effects are to be recognized.

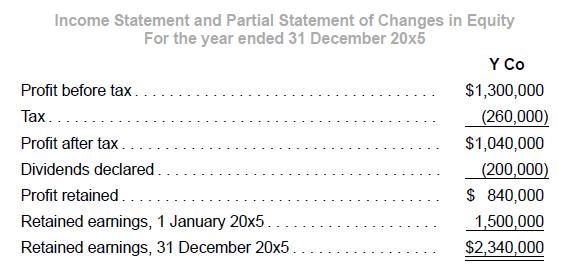

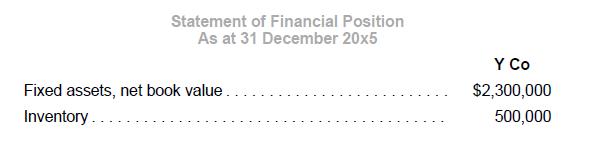

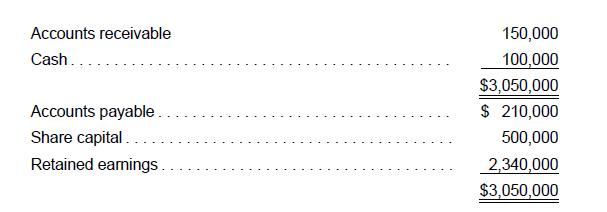

Extracts of Y Co’s financial statements for the year ended 31 December 20x5 are shown below:

Required:

1. Prepare the necessary consolidation adjustments for the year ended December 20x5.

2. Perform an analytical check on non-controlling interests as at 31 December 20x5.

3. If P Co measures non-controlling interests as a proportion of identifiable net assets as at acquisition date, prepare the consolidation adjustment(s) that differs from part 1, and perform an analytical check on noncontrolling interests’ balance as at 31 December 20x5.

Step by Step Answer:

Advanced Financial Accounting An IFRS Standards Approach

ISBN: 9781285428765

4th Edition

Authors: Pearl Tan, Chu Yeong Lim, Ee Wen Kuah