The partnership of Abbott, Robinson, and Stevens engaged you to adjust its accounting records and convert them

Question:

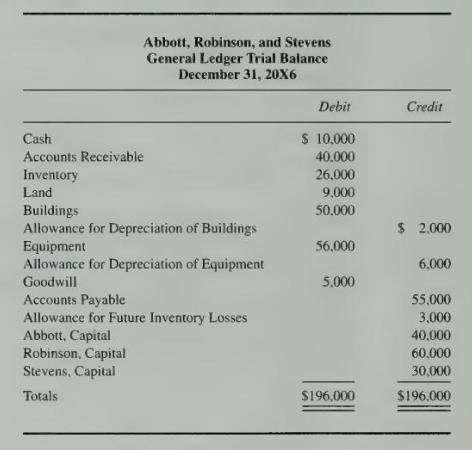

The partnership of Abbott, Robinson, and Stevens engaged you to adjust its accounting records and convert them uniformly to the accrual basis in anticipation of admitting Kingston as a new partner. Some accounts are on the accrual basis and others are on the cash basis. The partnership's books were closed at December 31, 20X6, by the bookkeeper, who prepared the general ledger trial balance that appears below.

Your inquiries disclosed the following:

1. The partnership was organized on January 1, 20X5, with no provision in the partnership agreement for the distribution of partnership profits and losses. During 20X5, profits were distributed equally among the partners. The partnership agreement was amended effective January 1, 20X6, to provide for the following profit and loss sharing ratio: Abbott, 50 percent; Robinson, 30 percent; and Stevens, 20 percent. The amended partnership agreement also stated that the accounting records were to be maintained on the accrual basis and that any adjustments necessary for 20X5 should be allocated according to the 20X5 distribution of profits.

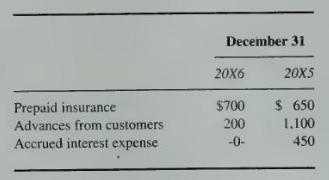

2. The following amounts were not recorded as prepayments or accruals:

The advances from customers were recorded as sales in the year the cash was received.

3. In 20X6, the partnership recorded a provision of \(\$ 3,000\) for anticipated declines in inventory prices. You convinced the partners that the provision was unnecessary and the provision and related allowance should be removed from the books.

4. The partnership charged equipment purchased for \(\$ 4,400\) on January 3, 20X6, to expense. The equipment has an estimated life of 10 years and an estimated salvage value of \(\$ 400\). The partnership depreciates its capitalized equipment on the double-declining-balance method.

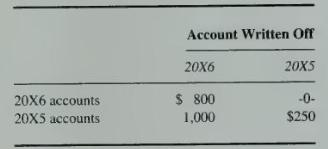

5. The partners agreed to establish an allowance for uncollectible accounts at 2 percent of current accounts receivable and 5 percent of past-due accounts. At December 31, 20X5, the partnership had \(\$ 54,000\) of accounts receivable, of which only \(\$ 4,000\) was past due. At December 31, 20X6, 15 percent of accounts receivable was past due, of which \(\$ 4,000\) represented sales made in 20X5 and was generally considered collectible. The partnership had written off uncollectible accounts in the year the accounts became worthless as follows:

6. Goodwill was recorded on the books in 20X6 and credited to the partners' capital accounts in the profit and loss sharing ratio in recognition of an increase in the value of the business resulting from improved sales volume. No amortization of goodwill was recorded. The partners agreed to write off the goodwill before admitting the new partner.

\section*{Required}

a. Prepare the journal entries to convert the accounting records to the accrual basis and to correct the books before admitting the new partner.

b. Without prejudice to your solution to part \(a\), assume that the assets were properly valued and that the adjusted total of the partners' capital account balances at December 31, 20X6, was \(\$ 140,000\). On that date, Kingston invested \(\$ 55,000\) in the partnership. Record the admission of Kingston using the goodwill method. Kingston is to be granted a one-fourth interest in the partnership. The other partners will retain their 50:30:20 income-sharing ratio for the remaining three-fourths' interest.

Step by Step Answer:

Advanced Financial Accounting

ISBN: 9780072444124

5th Edition

Authors: Richard E. Baker, Valdean C. Lembke, Thomas E. King