Organizations often will utilize third parties to perform their resource management processes. For example, organizations can utilize

Question:

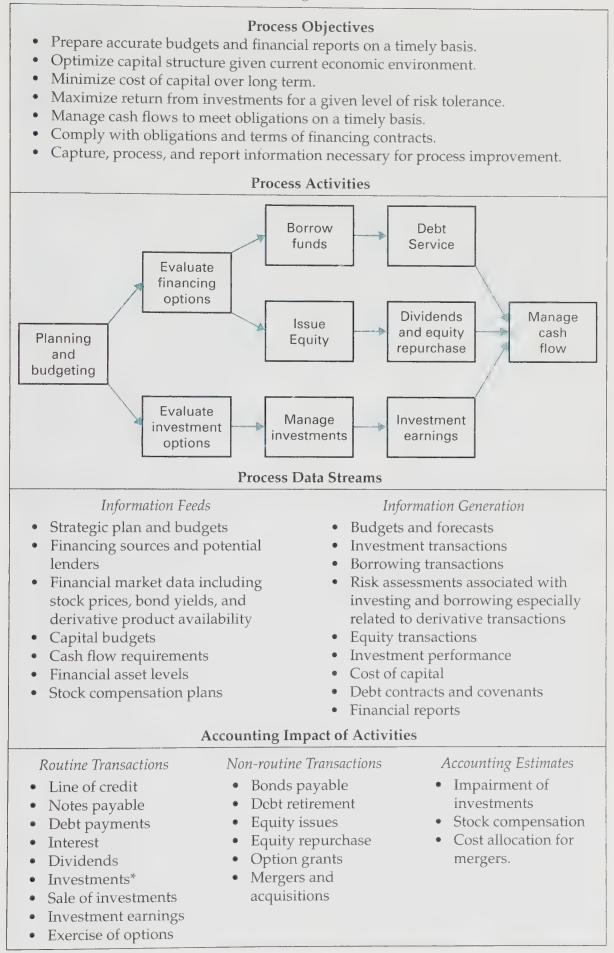

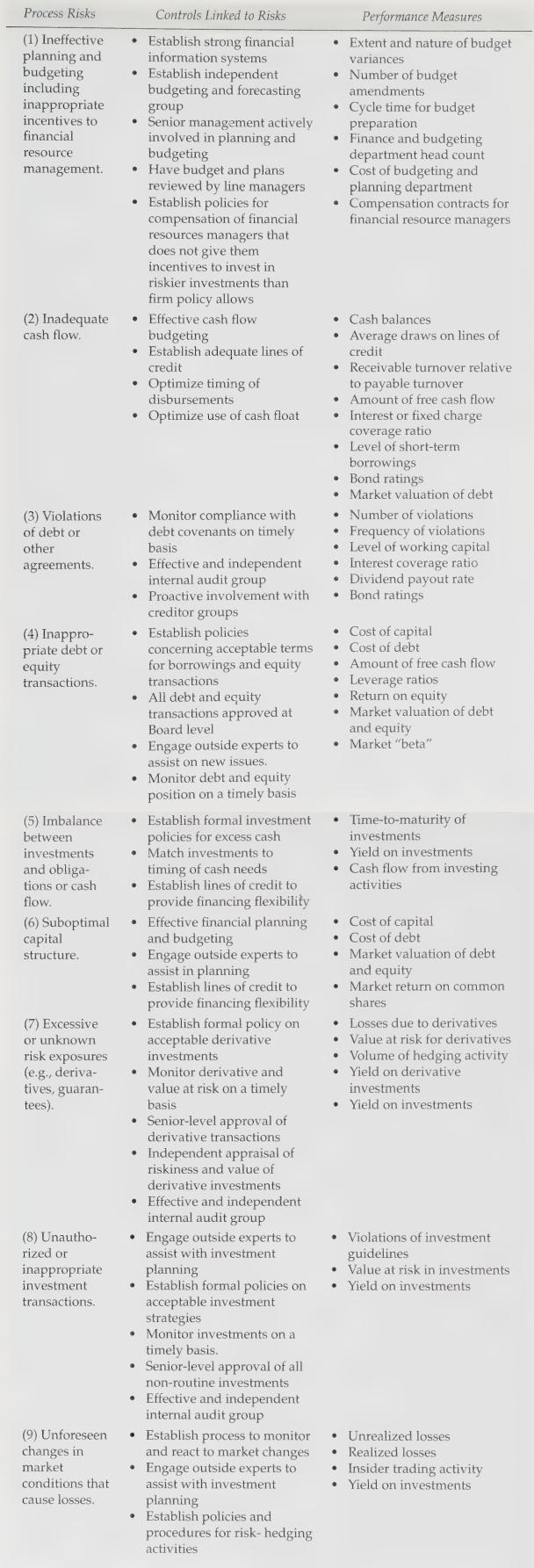

Organizations often will utilize third parties to perform their resource management processes. For example, organizations can utilize investment banks to perform financial asset management to conduct many of the activities shown in Figure 13-6. Access Credit Suisse's web site and research the descriptions and product offerings under asset management. Use this information and Figures 13-6 and Figure 13-7 to create an internal threat analysis for organizations that opt to use Credit Suisse to perform financial resource management.

Figure 13-6

Figure 13-7

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Branice Buyengo Ajevi

I have been teaching for the last 5 years which has strengthened my interaction with students of different level.

1+ Reviews

10+ Question Solved

Related Book For

Auditing Assurance And Risk

ISBN: 9780324313185

3rd Edition

Authors: W. Robert Knechel, Steve Salterio, Brian Ballou

Question Posted: