Exercise 2.14 (Chebyshevs Inequality) Suppose that a random variable X has the mean = E[X] and

Question:

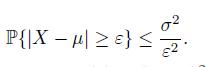

Exercise 2.14 (Chebyshev’s Inequality) Suppose that a random variable X has the mean μ = E[X] and the variance σ2 = V[X]. For any ε > 0, prove that

Hint: Use Markov’s inequality with h(x) = (x − μ)2 and a = ε2.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Khurram shahzad

I am an experienced tutor and have more than 7 years’ experience in the field of tutoring. My areas of expertise are Technology, statistics tasks I also tutor in Social Sciences, Humanities, Marketing, Project Management, Geology, Earth Sciences, Life Sciences, Computer Sciences, Physics, Psychology, Law Engineering, Media Studies, IR and many others.

I have been writing blogs, Tech news article, and listicles for American and UK based websites.

5+ Reviews

17+ Question Solved

Related Book For

Stochastic Processes With Applications To Finance

ISBN: 9781439884829

2nd Edition

Authors: Masaaki Kijima

Question Posted: