Exercise 5.8 In the risk exchange market considered in Section 5.4, suppose that the expected utility is

Question:

Exercise 5.8 In the risk exchange market considered in Section 5.4, suppose that the expected utility is given by

Suppose further that there is η > 0 such that π(Y ) = EP[ηY ] and EP[η] = 1, and that the utility functions are exponential (u′

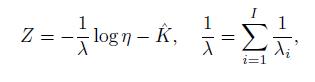

i(x) = e−λix). Consider then the Lagrange equation

![]()

Prove the following.

(1) Calculate the first-order condition with respect to Y (ω) to maximize L, and show that

where Yi is the optimal risk exchange.

(2) Show that the market clearing condition implies

for some ˆK .

(3) Show that η = Ke−λZ and K = (EP[e−λZ])−1.

For the general case, see B¨uhlmann (1983) and Iwaki, Kijima, and Morimoto (2001).

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Muhammad Ghyas Asif

It is my obligation to present efficient services to my clients by providing a work of quality, unique, competent and relevant. I hope you have confidence in me and assign me the order and i promise to follow all the instructions and keep time.

109+ Reviews

203+ Question Solved

Related Book For

Stochastic Processes With Applications To Finance

ISBN: 9781439884829

2nd Edition

Authors: Masaaki Kijima

Question Posted: