Question:

Corporation tax for financial years 19X1, 19X2, and 19X3 was 35 per cent, the ACT rate was 20 per cent and income tax for each year was 25 per cent.

You are required to enter up the following accounts for the year ended 31 December 19X2 for Barnet Ltd: Deferred tax; Income tax; Interest receivable; Debenture interest; Franked investment income; Advance corporation tax; Corporation tax; Tax on profit on ordinary activities; Preference dividends; Ordinary dividends; Profit and loss account extract. Also Balance sheet extracts as at 31 December 19X2.

A typical professional examination question. It is not easy. Remember to bring forward the balances from the previous year which will often have to be deduced. The letters (A) to (N) against the information will make it easier for you to check your answer against that given at the back of the book.

Transcribed Image Text:

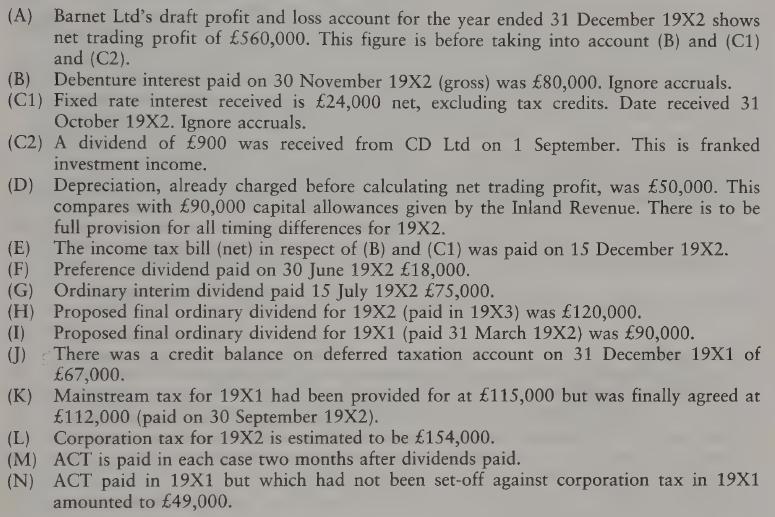

(A) Barnet Ltd's draft profit and loss account for the year ended 31 December 19X2 shows net trading profit of 560,000. This figure is before taking into account (B) and (C1) and (C2). (B) Debenture interest paid on 30 November 19X2 (gross) was 80,000. Ignore accruals. (C1) Fixed rate interest received is 24,000 net, excluding tax credits. Date received 31 October 19X2. Ignore accruals. (C2) A dividend of 900 was received from CD Ltd on 1 September. This is franked investment income. (D) Depreciation, already charged before calculating net trading profit, was 50,000. This compares with 90,000 capital allowances given by the Inland Revenue. There is to be full provision for all timing differences for 19X2. (E) The income tax bill (net) in respect of (B) and (C1) was paid on 15 December 19X2. (F) Preference dividend paid on 30 June 19X2 18,000. (G) Ordinary interim dividend paid 15 July 19X2 75,000. (H) Proposed final ordinary dividend for 19X2 (paid in 19X3) was 120,000. (I) Proposed final ordinary dividend for 19X1 (paid 31 March 19X2) was 90,000. (J) There was a credit balance on deferred taxation account on 31 December 19X1 of 67,000. (K) Mainstream tax for 19X1 had been provided for at 115,000 but was finally agreed at 112,000 (paid on 30 September 19X2). (L) Corporation tax for 19X2 is estimated to be 154,000. (M) ACT is paid in each case two months after dividends paid. (N) ACT paid in 19X1 but which had not been set-off against corporation tax in 19X1 amounted to 49,000.