For the LM Co. Ltd, who produce a standard type of product, you are required to prepare

Question:

For the LM Co. Ltd, who produce a standard type of product, you are required to prepare at 1 January 1985 for each of the three months January, February and March 1985:

(a) a budget of sales;

(b) a budget of production, bought-out products, and stock of finished goods;

(c) a budget of purchases of raw materials;

(d) a statement showing the expected manufacturing contribution from sales if the above budgets are achieved and if costs are at standard.

The following data about the company are available:

(1) Sales

(1) On 1 December each year the total sales for the ensuing year are estimated. Monthly sales are then budgeted by use of the pattern given in (iii) below.

(ii) During the 11 months to 30 November 1984 sales were 21,800 units.

Sales in December 1984 were expected to be 2,200 units. For 1985 as a whole a 20 per cent increase over 1984 is expected.

(iii) The pattern of the company's sales is that 5 per cent of the annual total are made in each month except in:

February, when 8% of annual sales are made March, when 22% of annual sales are made July, when 20% of annual sales are made September, when 10% of annual sales are made

(2) Production

(i) The output capacity of the plant is 2,000 units per month.

(ii) Work put in hand one month is delivered to finished goods stores in the following month.

(iii) Raw material purchases are scheduled so that the material required for each month is on hand at the beginning of that month.

(3) Stocks and bought-out units (i) The minimum stock level is 5 per cent of the total sales for the previous year. This is also the desired level, but for seasonal requirements it may be built up by production to a maximum of 15 per cent of the previous year's sales.

(ii) If requirements for sales are above what production and stocks permit, it is possible to buy-out extra requirements for delivery in the month in which the goods are to be sold. The standard cost of such bought-out goods is £55 per unit.

(iii) Finished stock on 1 January 1985 is expected to be 2,500 units, all of which have been produced in the plant. The company operates a first in, first-out system for its finished stock, but regards finished goods of its own production in any month as having been received before units bought-out during that month.

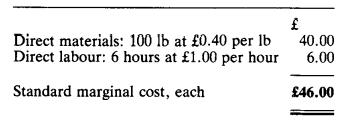

(4) Selling price and marginal cost T he product sells at £80 each; its standard marginal cost, when produced in the factory, is as follows:

There is no variable overhead.

Step by Step Answer: