Flexible budget; overhead variance analysis LO 2 Presented below are the monthly factory overhead cost budget (at

Question:

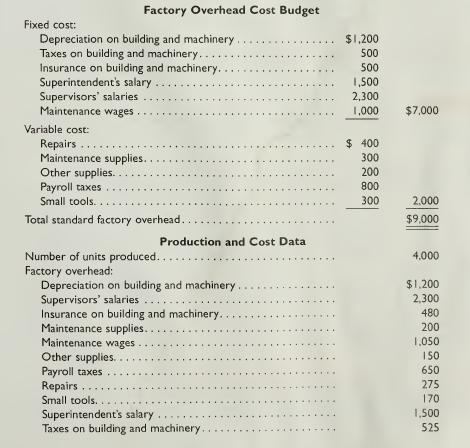

Flexible budget; overhead variance analysis LO2 Presented below are the monthly factory overhead cost budget (at normal capacity of 5,000 units or 20,000 direct labor hours) and the production and cost data for a month.

Required:

1.Assuming that variable costs will vary in direct proportion to the change in volume, prepare a flexible budget for production levels of 80, 90, and I 10%. Also determine the rate for application of factory overhead to work in process at each level of volume.

2. Prepare a flexible budget for production levels of 80, 90, and I 1 0%, assuming that variable costs will vary in direct proportion to the change in volume, but with the following exceptions: (Hint: Set up a third category for semifixed expenses.)

a. At 110% of capacity, an assistant department head will be needed at a salary of $10,500 annually.

b. At 80% of capacity, the repairs expense will drop to one-half of the amount at 100% capacity.

c. Maintenance supplies expense will remain constant at all levels of production.

d. At 80% of capacity, one part-time maintenance worker, earning $6,000 a year, will be laid off.

e. At 110% of capacity, a machine not normally in use and on which no depreciation is normally recorded will be used in production. Its cost was $12,000 and it has a ten-year life.

3. Using the flexible budget prepared in (I), determine the budgeted cost at 96% of capacity, using interpolation.

4. Using the flexible budget prepared in (I), determine the budgeted cost at 104% of capacity using a method other than interpolation.

Step by Step Answer: