Stores pricing and preparation of relevant ledger accounts V Ltd operates interlocking financial and cost accounts. The

Question:

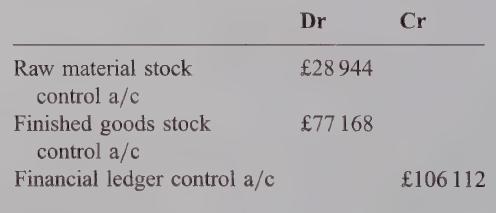

Stores pricing and preparation of relevant ledger accounts V Ltd operates interlocking financial and cost accounts. The following balances were in the cost ledger at the beginning of a month, the last month (Month 12) of the financial year:

There is no work in progress at the end of each month.

21600 kilos of the single raw material were in stock at the beginning of Month 12. Purchases and issues during the month were as follows:

A weighted average price per kilo (to four decimal places of a £) is used to value issues of raw material to production. A new average price is determined after each material purchase, and issues are charged out in total to the nearest £.

Costs of labour and overhead incurred during Month 12 were £35407. Production of the company’s single product was 17 150 units.

Transfers from finished goods stocks on sale of the product are made on a FIFO basis.

Required:

(a) Prepare the raw material stock control account, and the finished goods stock control account, for Month 12. (Show detailed workings to justify the summary entries made in the accounts.) (12 marks)

(b) Explain the purpose of the financial ledger control account. (4 marks)

(c) Prepare the raw material usage and the raw material purchases budgets for the year ahead (in kilos) using the following information where relevant:

Sales budget, 206000 units.

Closing stock of finished goods at the end of the budget year should be sufficient to meet 20 days sales demand in the year following that, when sales are expected to be 10%

higher in volume than in the budget year.

Closing stock of raw materials should be sufficient to produce 11700 units.

(NB You should assume that production efficiency will be maintained at the same level, and that there are 250 working days in each year.)

Step by Step Answer: