You are given: (i) An investor short-sells a nondividend-paying stock that has a current price of 44

Question:

You are given:

(i) An investor short-sells a nondividend-paying stock that has a current price of 44 per share.

(ii) This investor also writes a collar on this stock consisting of a 40-strike European put option and a 50-strike European call option. Both options expire in one year.

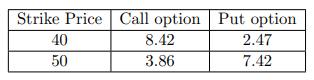

(iii) The prices of the options on this stock are:

(iv) The continuously compounded risk-free interest rate is 5%.

(v) Assume there are no transaction costs.

Calculate the maximum profit for the overall position at expiration.

(A) 2.61

(B) 3.37

(C) 4.79

(D) 5.21

(E) 7.39

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

C The written collar consists of a short 40strike put and a long 50strike call The i...View the full answer

Answered By

Issa Shikuku

I have vast experience of four years in academic and content writing with quality understanding of APA, MLA, Harvard and Chicago formats. I am a dedicated tutor willing to hep prepare outlines, drafts or find sources in every way possible. I strive to make sure my clients follow assignment instructions and meet the rubric criteria by undertaking extensive research to develop perfect drafts and outlines. I do this by ensuring that i am always punctual and deliver quality work.

6+ Reviews

13+ Question Solved

Related Book For

Question Posted: