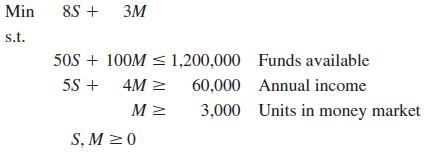

Question: Recall the Innis Investments problem (Chapter 7, Problem 39). Letting S = units purchased in the stock fund M = units purchased in the money

Recall the Innis Investments problem (Chapter 7, Problem 39). Letting

S = units purchased in the stock fund

M = units purchased in the money market fund

leads to the following formulation:

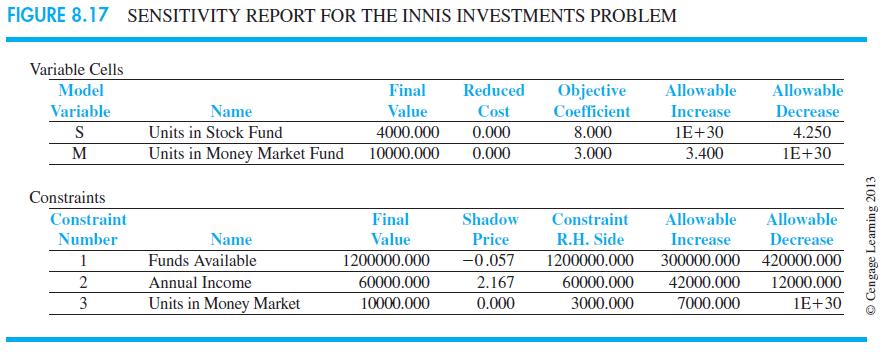

The sensitivity report is shown in Figure 8.17.

a. What is the optimal solution, and what is the minimum total risk?

b. Specify the objective coefficient ranges.

c. How much annual income will be earned by the portfolio?

d. What is the rate of return for the portfolio?

e. What is the shadow price for the funds available constraint?

f. What is the marginal rate of return on extra funds added to the portfolio?

Step by Step Solution

3.36 Rating (162 Votes )

There are 3 Steps involved in it

Solutions Step 1 Ans So we have given an lpp Min 8 S 3 M st 50 S 100 M 1200000 Funds available 5 S 4 M 60000 Annual income M 3000 Units in money marke... View full answer

Get step-by-step solutions from verified subject matter experts