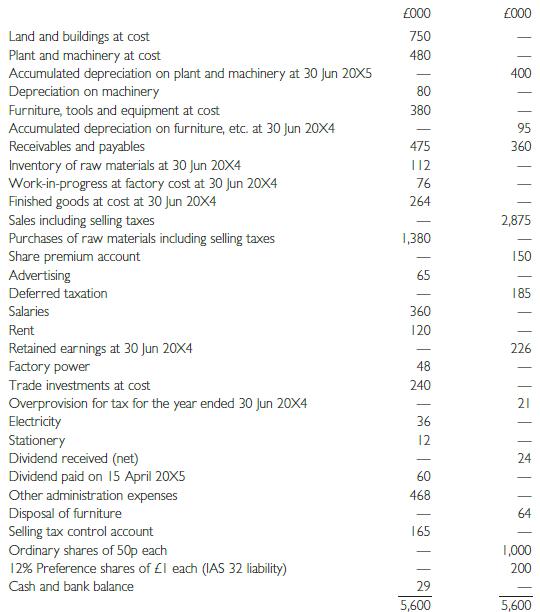

Cryptic plc extracted its trial balance on 30 June 20X5 as follows: The following information is relevant:

Question:

Cryptic plc extracted its trial balance on 30 June 20X5 as follows:

The following information is relevant:

(i) The company discontinued a major activity during the year and replaced it with another. All noncurrent assets involved in the discontinued activity were redeployed for the new one. The following expenses incurred in this respect, however, are included in ‘Other administration expenses’:

£000 Cancellation of contracts re terminated activity 165 Fundamental reorganisation arising as a result 145 Cryptic has decided to present its results from discontinued operations as a single line on the face of the income statement with analysis in the notes to the accounts as allowed by IFRS 5.

(ii) On 1 Januar y 20X5 the company acquired new land and buildings for £150,000. The remainder of land and buildings, acquired nine years earlier, have NOT been depreciated until this year.

The company has decided to depreciate the buildings, on the straight-line method, assuming that one-third of the cost relates to land and that the buildings have an estimated economic life of 50 years. The company policy is to charge a full year of depreciation in the year of purchase and none in the year of sale.

(iii) Plant and machiner y was all acquired on 1 July 20X0 and has been depreciated at 10% per annum on the straight-line method. The estimate of useful economic life had to be revised this year when it was realised that if the market share is to be maintained at current levels, the company has to replace all its machiner y by 1 July 20X6. The balance in the ‘Accumulated provision for depreciation’ account on 1 July 20X4 was amended to reflect the revised estimate of useful economic life and the impact of the revision adjusted against the retained earnings brought for ward from prior years.

(iv) Furniture acquired for £80,000 on 1 January 20X3 was disposed of for £64,000 on 1 April 20X5. Furniture, tools and equipment are depreciated at 5% p.a. on cost. Depreciation for the current year has not been provided.

(v) Results of the inventor y counting at year-end are as follows:

Inventor y of raw materials at cost including selling tax £197,800 Work-in-progress at factor y cost £54,000 Finished goods at cost £364,000 (vi) The company allocates its expenditure as follows:

(vii) The directors wish to make an accrual for audit fees of £18,000 and estimate the income tax for the year at £65,000. £11,000 should be transferred from the deferred tax account. The directors have to pay the preference dividend.

(viii) The following analysis has been made:

New activity Discontinued activity Sales excluding selling taxes £165,000 £215,000 Cost of sales £98,000 £155,000 Distribution cost £16,500 £48,500 Administrative expenses £22,500 £38,500 (ix) Assume that selling taxes applicable to all purchases and sales is 15%, the basic rate of personal income tax is 25% and the corporate income tax rate is 35%.

Required:

(a) Advise the company on the accounting treatment in respect of information stated in (ii) above.

(b) In respect of the information stated in (iii) above, state whether a company is permitted to revise its estimate of the useful economic life of a non-current asset and comment on the appropriateness of the accounting treatment adopted.

(c) Set out a statement of movement of property, plant and equipment in the year to 30 June 20X5.

(d) Set out for publication the income statement for the year ended 30 June 20X5, the balance sheet as at that date and any notes other than that on accounting policy, in accordance with relevant standards.

Step by Step Answer:

Financial Accounting And Reporting

ISBN: 9780273712312

12th Edition

Authors: Barry Elliott, Jamie Elliott