Olive A/S, incorporated with an authorised capital consisting of one million ordinar y shares of 1 each,

Question:

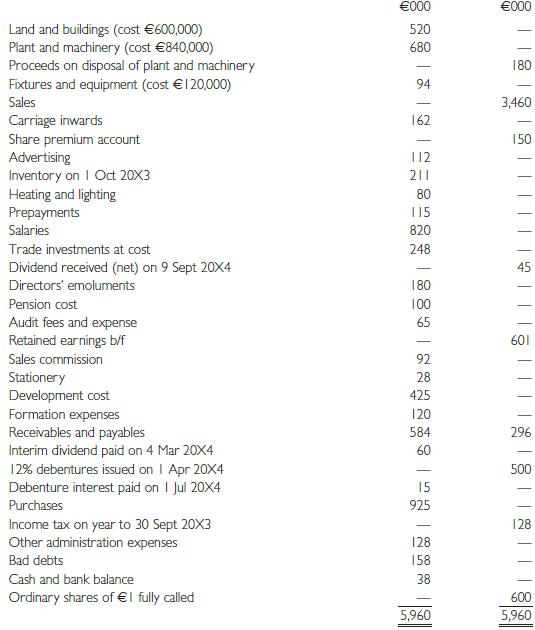

Olive A/S, incorporated with an authorised capital consisting of one million ordinar y shares of €1 each, employs 646 persons, of whom 428 work at the factor y and the rest at the head office. The trial balance extracted from its books as at 30 September 20X4 is as follows:

You are informed as follows:

(a) As at 1 October 20X3 land and buildings were revalued at €900,000. A third of the cost as well as all the valuation is regarded as attributable to the land. Directors have decided to repor t this asset at valuation.

(b) New fixtures were acquired on 1 Januar y 20X4 for €40,000; a machine acquired on 1 October 20X1 for €240,000 was disposed of on 1 July 20X4 for €180,000, being replaced on the same date by another acquired for €320,000.

(c) Depreciation for the year is to be calculated on the straight-line basis as follows:

Buildings: 2% p.a.

Plant and machiner y: 10% p.a.

Fixtures and equipment: 10% p.a.

(d) Inventor y in trade, including raw materials and work-in-progress on 30 September 20X4, has been valued at cost at €364,000.

(e) Prepayments are made up as follows:

€000 Amount paid in advance for a machine 60 Amount paid in advance for purchasing raw materials 40 Prepaid rent 15 €115 (f ) In March 20X3 a customer had filed legal action claiming damages at €240,000. When accounts for the year ended 30 September 20X3 were finalised, a provision of €90,000 was made in respect of this claim. This claim was settled out of cour t in April 20X4 at €150,000 and the amount of the underprovision adjusted against the profit balance brought for ward from previous years.

(g) The following allocations have been agreed upon:

Factory Administration Depreciation of buildings 60% 40%

Salaries other than to directors 55% 45%

Heating and lighting 80% 20%

(h) Pension cost of the company is calculated at 10% of the emoluments and salaries.

(i) Income tax on 20X3 profit has been agreed at €140,000 and that for 20X4 estimated at €185,000. Corporate income tax rate is 35% and the basic rate of personal income tax 25%.

(j) Directors wish to write off the formation expenses as far as possible without reducing the amount of profits available for distribution.

Required:

Prepare for publication:

(a) The income statement of the company for the year ended 30 September 20X4, and

(b) the balance sheet as at that date along with as many notes (other than the one on accounting policy) as can be provided on the basis of the information made available.

Step by Step Answer:

Financial Accounting And Reporting

ISBN: 9780273712312

12th Edition

Authors: Barry Elliott, Jamie Elliott