Minicase 1 Morrow Snowboards} Snowboarding is a rapidly growing sport in the United States. Morrow Snowboards, located

Question:

Minicase 1 Morrow Snowboards}

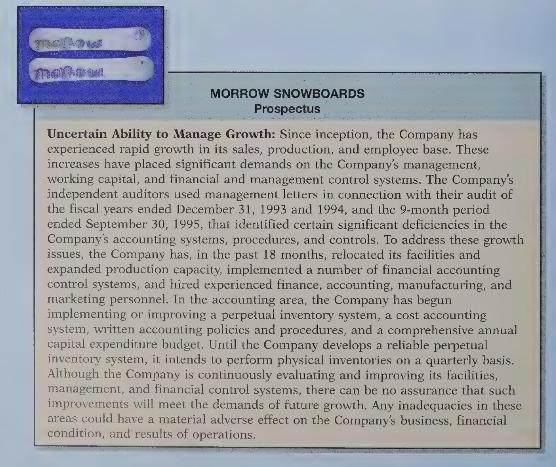

Snowboarding is a rapidly growing sport in the United States. Morrow Snowboards, located in Salem, Oregon, is a significant player in snowboard manufacture and sales. In 1995 Morrow announced it would sell shares of stock to the public. In its prospectus (an information-filled document that must be provided by every publicly traded U.S. firm the first time it issues shares to the public), Morrow disclosed the following information:

\section*{Instructions}

(a) What implications does this disclosure have for someone interested in investing in Morrow Snowboards?

(b) Do you think that the price of Morrow's stock will suffer because of these admitted deficiencies in its internal controls, including its controls over inventory?

(c) Why do you think Morrow decided to disclose this negative information?

(d) List the steps that Morrow has taken to improve its control systems.

(e) Do you think that these weaknesses are unusual for a rapidly growing company?

Step by Step Answer:

Financial Accounting Tools For Business Decision Making

ISBN: 9780471169192

1st Edition

Authors: Paul D. Kimmel, Jerry J. Weygandt, Donald E. Kieso