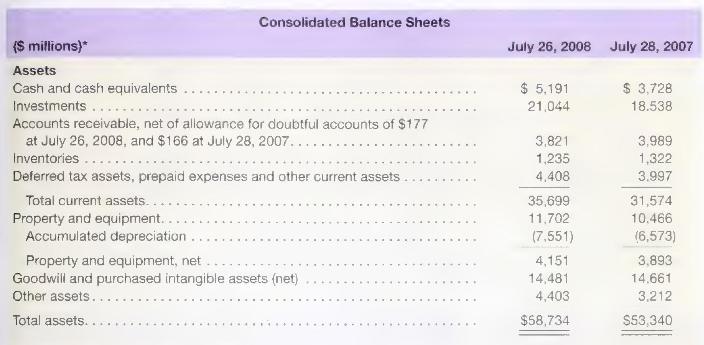

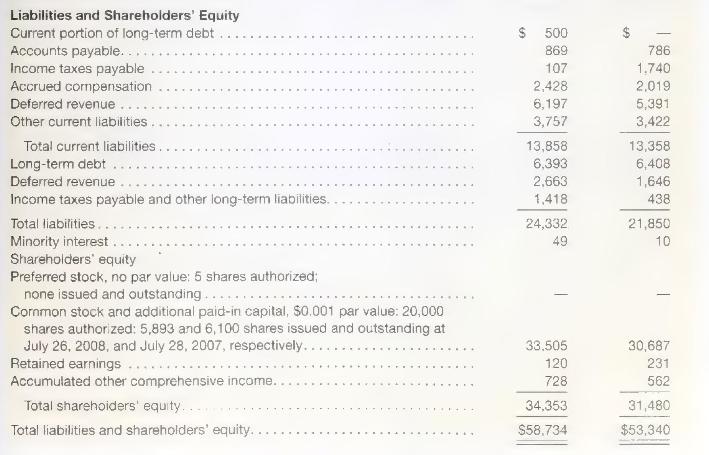

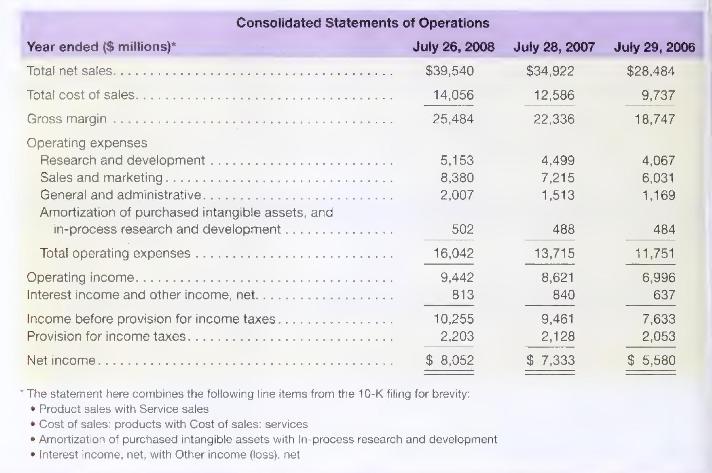

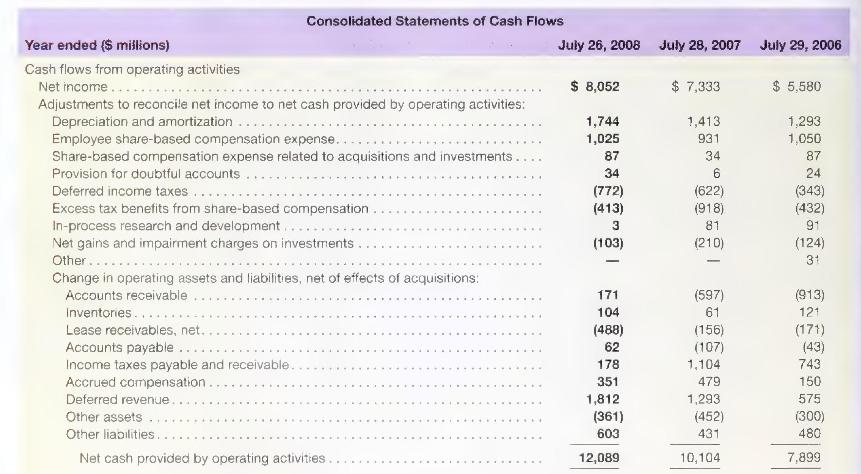

Following are the financial statements of Cisco Systems, Inc. footnotetext{ * Gross property and its accumulated depreciation

Question:

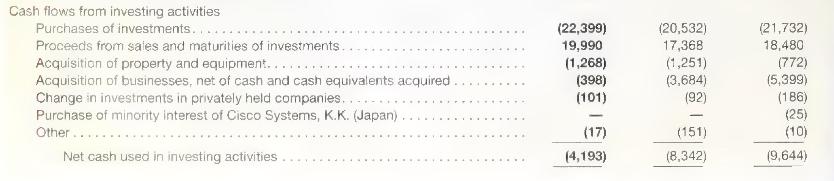

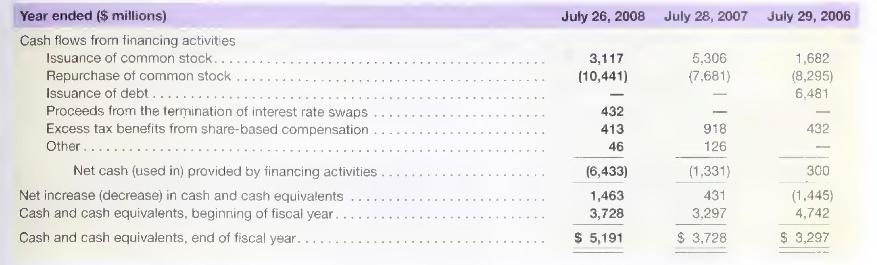

Following are the financial statements of Cisco Systems, Inc.

\footnotetext{

* Gross property and its accumulated depreciation are inserted in the balance sheet; both are taken from footnotes to financial statements. The balance sheet combines the following line items from the \(10-\mathrm{K}\) filing for brevity:

- Deferred tax assets with Prepaid expenses and other current assets - Goodwill with Purchased intangible assets, net - Noncurrent taxes payable with Other long-term liabilities }

The following is a breakdown of its depreciation and amortization expense.

Cisco provides the following footnote disclosures relating to its stock purchase program.

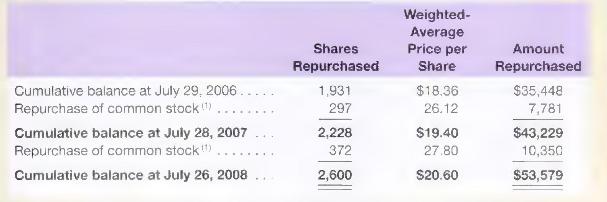

Stock Repurchase Program In September 2001, our Board of Directors authorized a stock repurchase program. As of July 26, 2008, our Board of Directors had authorized an aggregate repurchase of up to \(\$ 62\) billion of common stock under this program and the remaining authorized repurchase amount was \(\$ 8.4\) billion with no termination date. The stock repurchase activity under the stock repurchase program in fiscal 2007 and 2008 is summarized as follows (in millions, except per-share amounts):

The purchase price for the shares of our common stock repurchased is reflected as a reduction to shareholders' equity. In accordance with Accounting Principles Board Opinion No. 6, "Status of Accounting Research Bulletins," we are required to allocate the purchase price of the repurchased shares as (i) a reduction to retained earnings until retained earnings are zero and then as an increase to accumulated deficit and (ii) a reduction of common stock and additional paid-in capital. Issuance of common stock and the tax benefit related to employee stock incentive plans are recorded as an increase to common stock and additional paid-in capital. As a result of future repurchases, we may report an accumulated deficit as a component in shareholders' equity.

\section*{Required}

Forecast Cisco's 2009 and 2010 income statements, balance sheets, and statements of cash flows; round forecasts to \(\$\) millions. Using the same forecasting assumptions for both years; estimate forecasted income statement relations to 1 decimal (assume no change for: deferred tax and prepaid assets, other assets, other current liabilities, long-term debt, deferred revenue, long-term debt, long-term income taxes payable and other long-term liabilities, minority interest, common stock and additional paid-in capital. and accumulated other comprehensive income). Cisco's long-term debt footnote indicates no maturities of long-term debt until 2011. Forecast an increase in interest income from investment of any excess cash, whether included in cash and cash equivalents or in marketable securities, under the assumption that any excess cash is invested whether or not separately classified as investments on the balance sheet. What investment or financing assumptions are required for forecasting purposes? (Hint: Consider Cisco's stock repurchase footnote.) What is our assessment of Cisco's financial condition over the next two years?

Step by Step Answer:

Financial Accounting For MBAs

ISBN: 9781934319345

4th Edition

Authors: Peter D. Easton, John J. Wild, Robert F. Halsey, Mary Lea McAnally