Fine Linen Service began operations on January 28, 2014. The company does not establish an allowance for

Question:

July 6, 2014 Wrote off $10,000 as un-collectible from a sale made on March 1, 2014.

Feb. 3, 2015 Wrote off $50,000 as un-collectible from a sale made on October 28, 2014.

Mar. 11, 2016 Wrote off $25,000 as un-collectible from a sale made on December 20, 2014 ($12,000) and a sale made on May 10, 2014 ($13,000).

Mar. 24, 2016 Recovered $5,000 that had been written off on February 3, 2015. It is company policy to credit bad debt expense when an account is recovered.

Aug. 8, 2017 Wrote off $75,000 as un-collectible from sales made in 2014 ($20,000), in 2015 ($25,000), and in 2016 ($30,000).

Dec. 2, 2017 Wrote off $5,000 as un-collectible from a sale made on April 26, 2017.

Sept. 19, 2018 Wrote off $90,000 as un-collectible from sales in 2014 ($5,000), in 2015 ($30,000), in 2016 ($25,000), in 2017 ($20,000), and in 2018 ($10,000).

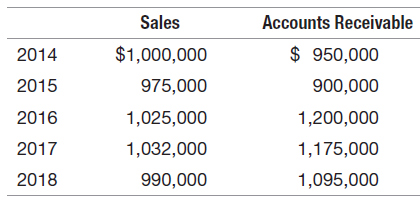

Over the period 2014 to 2018, Fine Linen Service realized the following sales and reported the following ending balances in accounts receivable.

At the beginning of operations, a consultant had informed Fine Linen Service that the company should expect not to collect 8 percent of total sales.

REQUIRED:

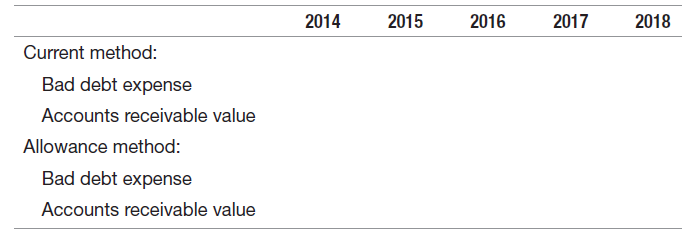

a. List the bad debt expense and the balance sheet value of accounts receivable for each year over the five year period under both Fine Linen€™s current method and the allowance method. Use the following format:

b. Compute the total bad debt expense over the five-year period under the two methods. Why is the allowance method preferred to Fine Linen€™s current method?

Balance SheetBalance sheet is a statement of the financial position of a business that list all the assets, liabilities, and owner’s equity and shareholder’s equity at a particular point of time. A balance sheet is also called as a “statement of financial...

Step by Step Answer:

a 2014 2015 2016 2017 2018 Current Method Bad debt expense 10000 50000 20000 a 80000 b 90000 AR Value 950000 900000 1200000 1175000 1095000 Allowance ...View the full answer