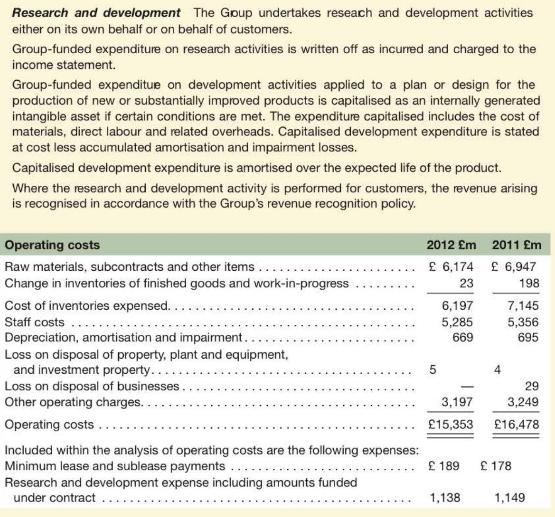

Headquartered in London in the United Kingdom, BAE Systems is a global defense, aerospace and security company

Question:

Headquartered in London in the United Kingdom, BAE Systems is a global defense, aerospace and security company employing around 88,200 people worldwide. The company's wide-ranging products and services cover air, land and naval forces, as well as advanced electronics, security, information technology, and support services. BAE Systems is the worlds̀ third largest defense and aerospace company based on revenues. The company uses IFRS for its financial statements, which include the following notes:

Required

a. Under IFRS, what six criteria did BAE Systems have to meet in order to capitalize development costs?

b. What was the common-sized research and development expense each year? The company recorded sales revenue of \(£ 17,834\) and \(£ 19,154\) in 2012 and 2011 respectively.

c. Assume that during 2012, the company capitalized \(£ 432\) of additional development expenditures and amortized \(£ 229\) of previously capitalized costs. Determine what the R\&D expense would have been under U.S. GAAP.

Step by Step Answer:

Financial And Managerial Accounting For MBAs

ISBN: 9781618533593

6th Edition

Authors: Peter D. Easton