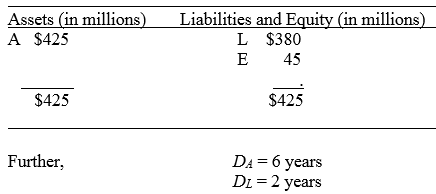

Dudley Hill Bank has the following balance sheet: The interest rate on both the assets and the

Question:

Dudley Hill Bank has the following balance sheet:

The interest rate on both the assets and the liabilities is 8 percent. The bank manager receives information from an economic forecasting unit that interest rates are expected to rise from 8 to 9 percent over the next six months.

a. Calculate the potential loss to Dudley Hill’s net worth (E) if the forecast of rising rates proves to be true.

b. Suppose the manager of Dudley Hill Bank wants to hedge this interest rate risk with T-bond futures contracts. The current futures price quote is $122.03125 per $100 of face value for the benchmark 20-year, and the minimum contract size is $100,000, so PF equals $122,031.25. The duration of the deliverable bond is 14.5 years. That is, DF = 14.5 years. How many futures contracts will be needed? Should the manager buy or sell these contracts? Assume no basis risk.

c. Verify that selling T-bond futures contracts will indeed hedge the FI against a sudden increase in interest rates from 8 to 9 percent, a 1 percent, interest rate shock.

d. If the bank had hedged with Eurodollar futures contracts that had a market value of $98 per $100 of face value, how many futures contracts would have been necessary to fully hedge the balance sheet?

e. How would your answer for part (b) change if the relationship of the price sensitivity of futures contracts to the price sensitivity of underlying bonds were br = 1.15?

f. Verify that selling T-bond futures contracts will indeed hedge the FI against a sudden increase in interest rates from 8 to 9 percent, a 1 percent, interest rate shock. Assume the yield on the T-bond underlying the futures contract is 8.45 percent as the bank enters the hedge and rates rise by 1.154792 percent.

Face ValueFace value is a financial term used to describe the nominal or dollar value of a security, as stated by its issuer. For stocks, the face value is the original cost of the stock, as listed on the certificate. For bonds, it is the amount paid to the...

Step by Step Answer:

a The bank could expect to lose 16574074 in shareholders net worth should the interest rate forecast ...View the full answer

Financial Institutions Management A Risk Management Approach

ISBN: 978-1259717772

9th edition

Authors: Anthony Saunders, Marcia Millon Cornett