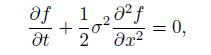

Let us consider the PDE with terminal condition In order to apply the representation theorem, we observe

Question:

Let us consider the PDE

with terminal condition

![]()

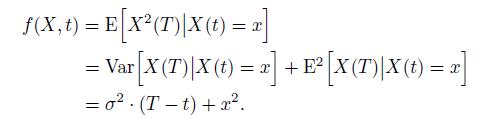

In order to apply the representation theorem, we observe that \(r=0\), \((x t)=\), and  , so that the underlying stochastic process boils down to a martingale described by

, so that the underlying stochastic process boils down to a martingale described by

![]()

Therefore, conditional on \(X(t)=x\), integration over the time interval \(\left[\begin{array}{ll}t, & T\end{array}\right]\) yields

where ![]() . Therefore,

. Therefore,

It is easy to check that this function satisfies the PDE and the terminal condition.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Milan Mondal

I am milan mondal have done my Msc in physics (special astrophysics and relativity) from the University of burdwan and Bed in physical science from the same University.

From 2018 I am working as pgt physics teacher in kendriya vidyalaya no2 kharagpur ,west bengal. And also I am doing advanced physics expert in chegg.com .also I teach Bsc physics .

I love to teach physics and acience.

If you give me a chance I will give my best to you.

4+ Reviews

10+ Question Solved

Related Book For

An Introduction To Financial Markets A Quantitative Approach

ISBN: 9781118014776

1st Edition

Authors: Paolo Brandimarte

Question Posted: