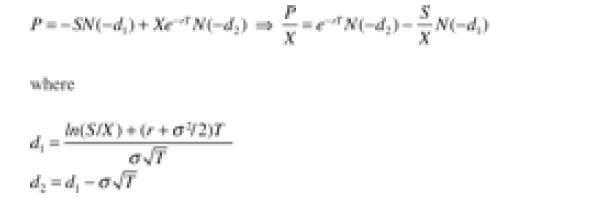

Note that you can also calculate the Black-Scholes put option premium as a percentage of the exercise

Question:

Note that you can also calculate the Black-Scholes put option premium as a percentage of the exercise price in terms of S/X:

a. Implement this in a spreadsheet or R.

b. Find the ratio of S/X for which C/ X and P/ X cross when T = 0.5, σ = 25%, r = 1%. (You can use a graph or you can use Excel’s Solver.) Note that this crossing point is affected by the interest rate and the option maturity, but not by σ.

Step by Step Answer:

This question has not been answered yet.

You can Ask your question!

Related Book For

Question Posted: