Suppose a share was priced at price P 0 at time 0, and suppose that at time

Question:

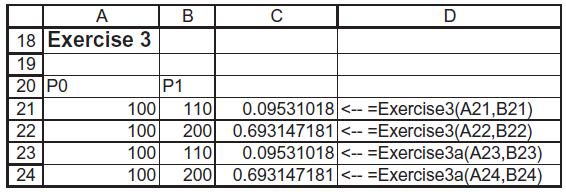

Suppose a share was priced at price P 0 at time 0, and suppose that at time 1 it will be priced P1. Then the continuously compounded return is defined as return = In(P1/P0). Implement this function in VBA. There are two ways to do this: You can use Worksheetfunction.Ln or the VBA function Log.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

ANSWER Here is a VBA function that calculates the continuously c...View the full answer

Answered By

Brian Kiprono

Taking part in public speeches, blogging, writing essays

0 Reviews

10+ Question Solved

Related Book For

Question Posted: