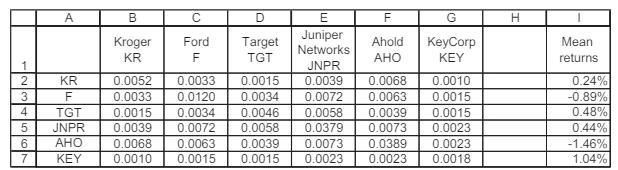

The following chart shows the variance-covariance matrix and the mean returns for six stocks. All the data

Question:

The following chart shows the variance-covariance matrix and the mean returns for six stocks. All the data are for monthly data (raw data are on the disk with the book).

a. Compute the global minimum variance portfolio (GMVP).

b. Compute the effi cient portfolio, assuming a monthly risk-free rate of 0.45%.

c. Show the frontier as the expected return and standard deviation of convex combinations of the GMVP and the efficient portfolio.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Kennedy Odhiambo

As a professional writer, I have been in the field for over 5 years having worked as a lecture in different tertiary institutions across the world. With this impeccable experience, I assure provision of a good and supporting environment for students to learn.

2+ Reviews

10+ Question Solved

Related Book For

Question Posted: