You have decided to create your own index of high-beta components of the DowJones 30 Industrials. Using

Question:

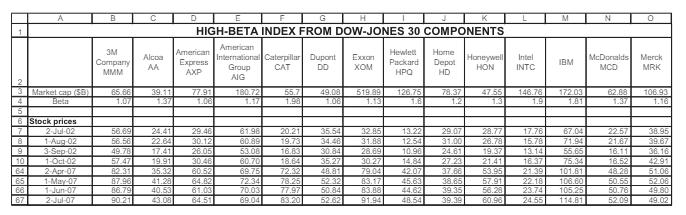

You have decided to create your own index of high-beta components of the DowJones 30 Industrials. Using Yahoo’s stock screener, you come up with the following data.

a. Compute the variance-covariance matrix of returns.

b. Assuming that the risk-free rate is 5.25% annually (=5.25%/12=0.44% monthly). and that the expected high-beta index annual return is 12% (= 1% monthly), compute the Black-Litterman monthly expected returns for each stock.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Nimlord Kingori

2023 is my 7th year in academic writing, I have grown to be that tutor who will help raise your grade and better your GPA. At a fraction of the cost on other sites, I will work on your assignment by taking it as mine. I give it all the attention it deserves and ensures you get the grade that I promise. I am well versed in business-related subjects, information technology, Nursing, history, poetry, and statistics. Some software's that I have access to are SPSS and NVIVO. I kindly encourage you to try me; I may be all that you have been seeking, thank you.

360+ Reviews

1070+ Question Solved

Related Book For

Question Posted: