Companies that want to manage their reported earnings can do so through real transactions that alter operating

Question:

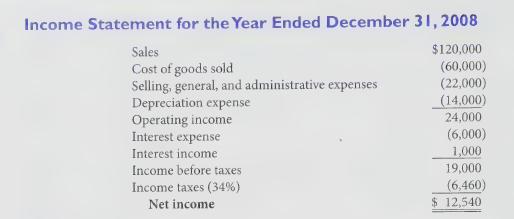

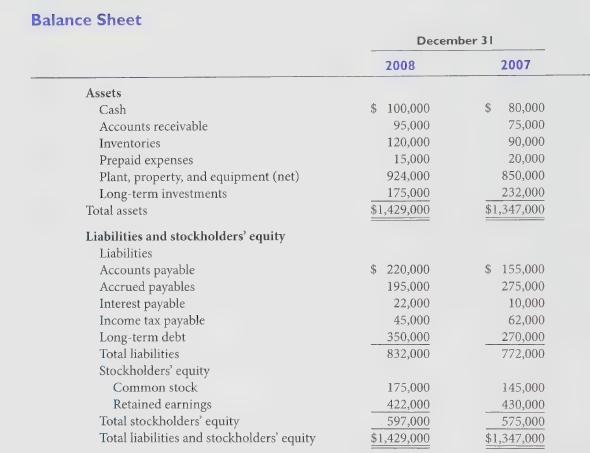

Companies that want to "manage" their reported earnings can do so through real transactions that alter operating cash flows or through accounting gimmicks that change only net income accruals (the noncash revenue and expense components of GAAP earnings). The 2007-2008 balance sheets and 2008 income statement of Runner's World follow. The company's operating cash flow for 2008 was ($38,460) a net outflow.

Required:

1. Calculate the net accruals (the difference between accrual earnings and operating cash flows) recorded by Runner’s World in 2008.

2. Identify the individual components of net accruals in requirement 1.

3. Which accruals identified in requirement 2 are subject to the greatest degree of management discretion?

4, Why might managers manipulate the firm’s discretionary accruals?

Step by Step Answer: