Refer to The Kroger Co. information in Case 15-3. Required: Explain how net benefit cost and OCI

Question:

Refer to The Kroger Co. information in Case 15-3.

Required:

Explain how net benefit cost and OCI would change if The Kroger Co. were using IAS 19.

Case 15-3.

The Kroger Co. operates numerous grocery store chains. Excerpts from Kroger’s Note 15 are presented below. The 2017 amounts are for the fiscal year ended February 3, 2018. All amounts are in millions of U.S. dollars. At February 3, 2018, Kroger had 870 million outstanding shares of common stock. Each share was trading at $29.34 at that time. Kroger had not yet adopted ASU 2017-07 in fiscal 2017.

15. COMPANY-SPONSORED BENEFIT PLANS

The Company administers non-contributory defined benefit retirement plans for some non-union employees and union-represented employees as determined by the terms and conditions of collective bargaining agreements.

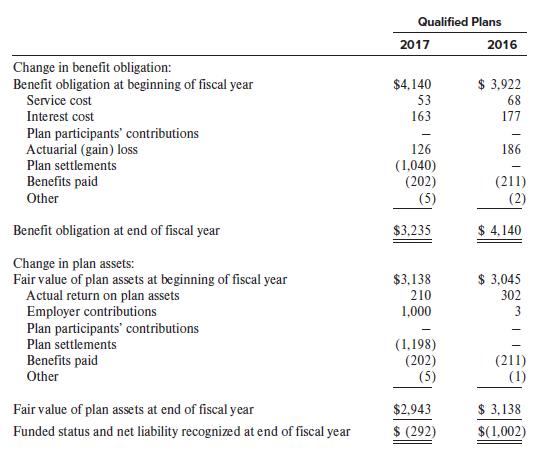

These include several qualified pension plans (the “Qualified Plans”) and non-qualified pension plans (the “Non-Qualified Plans”). The Non-Qualified Plans pay benefits to any employee that earns in excess of the maximum allowed for the Qualified Plans by Section 415 of the Internal Revenue Code. The Company only funds obligations under the Qualified Plans.

In 2017, the Company settled certain company-sponsored pension plan obligations using existing assets of the plan and a $1,000 contribution made to the plan in the third quarter of 2017.

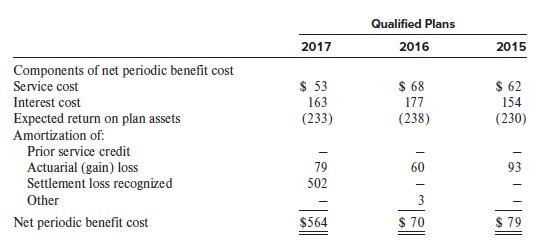

The Company recognized a settlement charge of approximately $502, $335 net of tax, associated with the settlement of the Company’s obligations for the eligible participants’ pension balances that were distributed out of the plan via a transfer to other qualified retirement plan options, a lump sum payout, or the purchase of an annuity contract, based on each participant’s election.

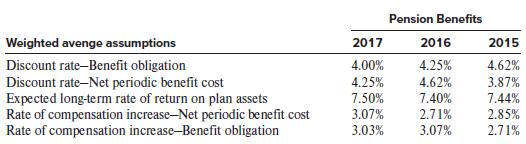

The Company’s 2017 assumed pension plan investment return rate was 7.50% compared to 7.40% in 2016 and 7.44% in 2015. The value of all investments in the company sponsored defined benefit pension plans during the calendar year ending December 31, 2017, net of investment management fees and expenses, increased 8.7%. Historically, the Company’s pension plans’ average rate of return was 5.7% for the 10 calendar years ended December 31, 2017, net of all investment management fees and expenses. For the past 20 years, the Company’s pension plans’ average annual rate of return has been 7.10%. At the beginning of 2017, to determine the expected rate of return on pension plan assets held by the Company for 2017, the Company considered current and forecasted plan asset allocations as well as historical and forecasted rates of return on various asset categories. Based on this information and forward looking assumptions for investments made in a manner consistent with its target allocations, which contemplates the Company’s transition to a liability driven investment (“LDI”) strategy, the Company believed a 7.50% rate of return assumption was reasonable for 2017.

The Company calculates its expected return on plan assets by using the market-related value of plan assets. The market-related value of plan assets is determined by adjusting the actual fair value of plan assets for gains or losses on plan assets. Gains or losses represent the difference between actual and expected returns on plan investments for each plan year. Gains or losses on plan assets are recognized evenly over a five year period. Using a different method to calculate the market-related value of plan assets would provide a different expected return on plan assets.

Step by Step Answer:

All referenced amounts are in millions 1 Kroger would still recognize its actuarial losses in OCIAOCI and record a liability on the balance sheet Howe...View the full answer

Financial Reporting And Analysis

ISBN: 9781260247848

8th Edition

Authors: Lawrence Revsine, Daniel Collins, Bruce Johnson, Fred Mittelstaedt, Leonard Soffer