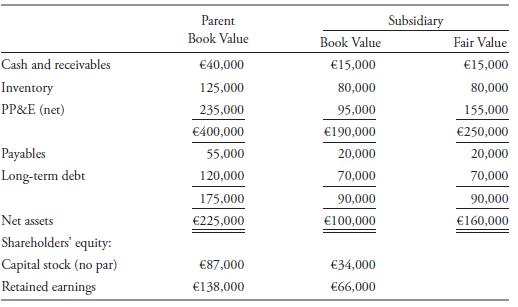

On 1 January 2012, the hypothetical Parent Co. acquired 90% of the outstanding shares of the hypothetical

Question:

On 1 January 2012, the hypothetical Parent Co. acquired 90% of the outstanding shares of the hypothetical Subsidiary Co. in exchange for shares of Parent Co.’s no par common stock with a fair value of €180,000. The fair market value of the subsidiary’s shares on the date of the exchange was €200,000. Below is selected fi nancial information from the two companies immediately prior to the exchange of shares (before the parent recorded the acquisition):

1. Calculate the value of PP&E (net) on the consolidated balance sheet under both IFRS and US GAAP.

2. Calculate the value of goodwill and the value of the non-controlling interest at the acquisition date under the full goodwill method.

3. Calculate the value of goodwill and the value of the non-controlling interest at the acquisition date under the partial goodwill method.

Step by Step Answer:

1 Relative to fair value the PPE of the subsidiary is understated by 60000 Under the acquisition method IFRS and US GAAP as long as the parent has con...View the full answer

International Financial Statement Analysis CFA Institute Investment Series

ISBN: 9780470287668

1st Edition

Authors: Thomas R. Robinson, Hennie Van Greuning CFA, Elaine Henry, Michael A. Broihahn, Sir David Tweedie