Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X)

Question:

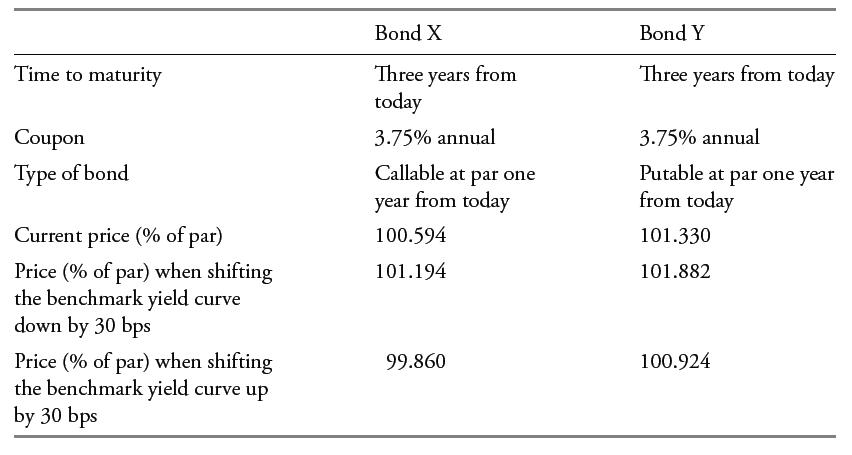

Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X) and a putable bond (Bond Y). She wants to examine the interest rate sensitivity of these two bonds to a parallel shift in the benchmark yield curve. Assuming an interest rate volatility of 10%, her valuation software shows how the prices of these bonds change for 30 bps shifts up or down: The price of Bond X is affected:

The price of Bond X is affected:

A. Only by a shift in the one-year par rate.

B. Only by a shift in the three-year par rate.

C. By all par rate shifts but is most sensitive to shifts in the one-year and three-year par rates.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

C is correct The main driver of the c...View the full answer

Answered By

Michael Mulupi

I am honest,hardworking, and determined writer

72+ Reviews

157+ Question Solved

Related Book For

Question Posted: