Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X)

Question:

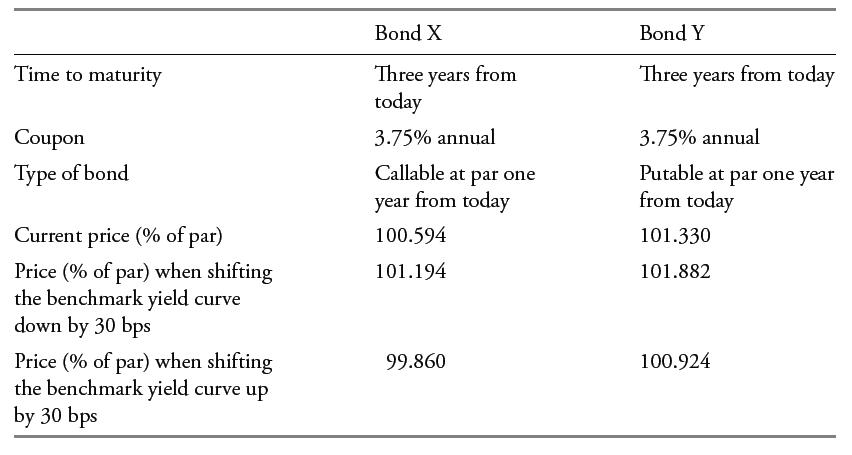

Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X) and a putable bond (Bond Y). She wants to examine the interest rate sensitivity of these two bonds to a parallel shift in the benchmark yield curve. Assuming an interest rate volatility of 10%, her valuation software shows how the prices of these bonds change for 30 bps shifts up or down: Which of the following statements is most accurate?

Which of the following statements is most accurate?

A. Bond Y exhibits negative convexity.

B. For a given decline in interest rate, Bond X has less upside potential than Bond Y.

C. The underlying option-free (straight) bond corresponding to Bond Y exhibits negative convexity.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

B is correct As interest rates decline the value of a call option increases whereas the val...View the full answer

Answered By

Deepak singh

I have completed my graduation from computer science engineering . I have good knowledge about programming language and love to solve many codes of any language. I have been an expert to other platforms too and have good experience of giving solution to the students of subject .

0 Reviews

10+ Question Solved

Related Book For

Question Posted: