At the monthly senior management meeting of Hampshire plc on 1 May 2010, various suggestions were made

Question:

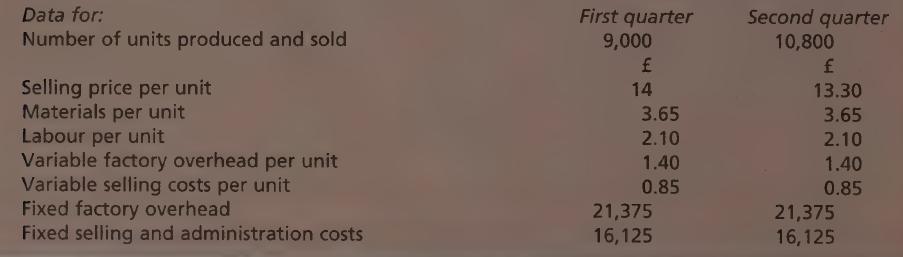

At the monthly senior management meeting of Hampshire plc on 1 May 2010, various suggestions were made to improve the profit to be made by selling the firm’s single product in the last quarter of the year ending 30 September 2010. The product is not subject to seasonal demand fluctuations, but there are several competitors producing similar items. In the first quarter of the year a suggestion was made that profit could be improved if the selling price were reduced by 5 per cent, and this was put into effect at the beginning of the second quarter. As the new price undercut that of the rival firms, demand increased, and the firm’s breakeven point was reduced.

The following suggestions have now been raised:

(i) Differentiate the product from its rivals by giving it a more distinctive shape, colour and packaging. This would increase material costs per unit by 0.30, but selling price would not be raised. Demand is then predicted to rise by 10 per cent;

(ii) Improve the quality of the product by strengthening it and giving it a one-year guarantee - material costs would then increase by 0.15 per unit and labour costs by 0.30 per unit. Selling price would rise by 0.40 per unit, and demand increase by 7 per cent;

(iii) Further reduce the selling price by 10 per cent - demand to rise by 20 per cent;

(iv) Pay commission plus salaries instead of fixed salaries only to all sales staff. Variable selling costs would then rise by 0.20 per unit, but fixed costs would fall by 4,100 per quarter;

(v) Subcontract the making of some components, and close the department responsible, making six staff redundant at an estimated cost to the firm of 12,000. 30,000 components are currently made per quarter. Each component's variable cost is 0.55. They can be bought from a recently established firm for 0.60 per unit. The department's share of the firm's fixed costs is 20 per cent and 2,500 fixed costs per quarter would cease to arise if the department were to be closed.

Required:

A. Calculate the profit made i in each of the first and second quarters, showing clearly the contribution per unit in each case.

B. Draw one breakeven chart showing the total costs and total revenues for the first and second quarters. You should label clearly the two breakeven points and margins of safety.

C. Taking each suggestion independently, calculate the profit that might be made in the last quarter if each of them were to be implemented.

D. Discuss the implications for the firm of undertaking suggestions (/)-(iv), and for the firm and the local community of undertaking suggestion (v).

E. Explain to the senior managers how, while breakeven analysis is useful, it has limitations.

Step by Step Answer:

Business Accounting Uk Gaap Volume 2

ISBN: 9780273718802

1st Edition

Authors: Alan Sangster, Frank Wood