CK Ltd was incorporated on 15 December 2009 with an authorised capital of 200,000 ordinary shares of

Question:

CK Ltd was incorporated on 15 December 2009 with an authorised capital of 200,000 ordinary shares of £0.20 each to acquire as at 31 December 2009 the business of CK, a sole trader, and RP Ltd, a company.

From the following information you are required to prepare:

(a) the realisation and capital accounts in the books of CK and RP Ltd showing the winding up of these two concerns;

(b) the journal entries to open the books of CJK Ltd, including cash transactions and the raising of finance;

(c) the balance sheet of CJK Ltd after the transactions have been completed.

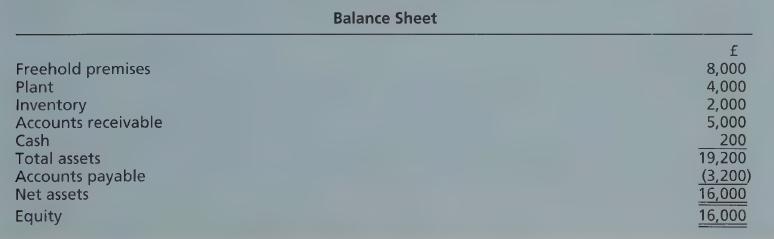

The balance sheet of CK as at 31 December 2009 is as follows:

The assets (excluding cash) and the liabilities were taken over at the following values: freehold premises £10,000; plant £3,500; inventory £2,000; accounts receivable £5,000 less an allowance for doubtful debts of £300; goodwill £7,000; accounts payable £3,200 less a discount provision of £150.

The purchase consideration, based on these values, was settled by the issue of shares at par.

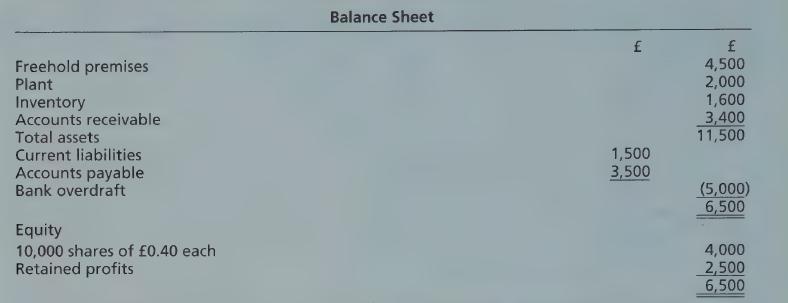

The balance sheet of RP Ltd as at 31 December 2009 is as follows:

The assets and liabilities were taken over at book value with the exception of the freehold premises which were revalued at £5,500. The purchase consideration was a cash payment of £1 and three shares in CJK Ltd at par in exchange for every two shares in RP Ltd.

Additional working capital and the funds required to complete the purchase of RP Ltd were provided by the issue for cash of:

(i) 10,000 shares at a premium of £0.30 per share;

(ii) £8,000 7% loan notes at 98.

The expenses of incorporating CJK Ltd were paid, amounting to £1,200.

(Chartered Institute of Management Accountants)

Step by Step Answer:

Frank Woods Business Accounting Volume 2

ISBN: 9780273712138

11th Edition

Authors: Frank Wood, Alan Sangster