Use the data in exercise E5-26 to journalize the following for the periodic system: 1. Total October

Question:

Use the data in exercise E5-26 to journalize the following for the periodic system:

1. Total October purchases in one summary entry. All purchases were on credit.

2. Total October sales in a summary entry. Assume that the selling price was \(\$ 300\) ) per unit and that all sales were on credit.

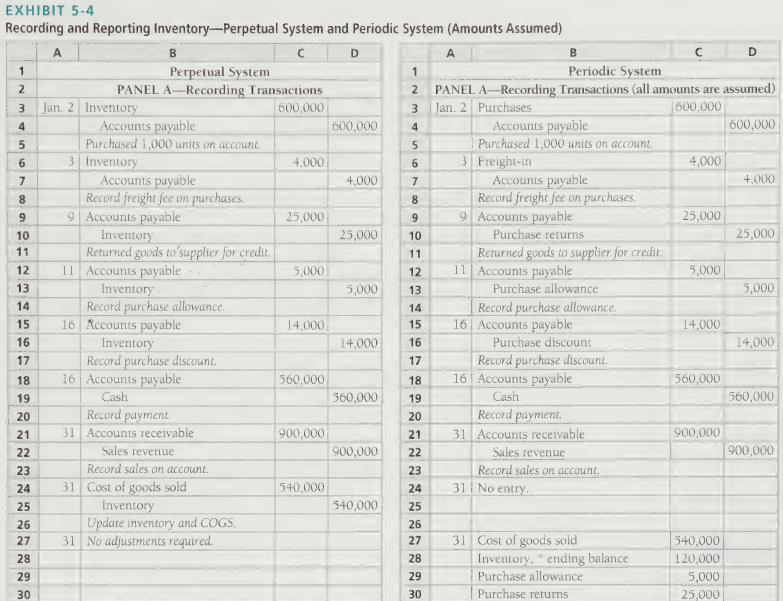

3. October 31 entries for inventory. The company uses weighted-average cost. Post to the Cost of Goods Sold T-account to show how this amount is determined. Label each item in the account 4. Show the computation of cost of goods sold using the example given in Exhibit 5-4, Panel B.

5. Assume it is year end. Prepare the journal entries to update the inventory records.

Exercise 5-26

Suppose a technology company's inventory records for a particular computer chip indicate the following at October 31 :

The physical count of inventory at October 31 indicates that 8 units of inventory are on hand.

Step by Step Answer:

Financial Accounting

ISBN: 9780135433065

7th Canadian Edition

Authors: Walter Harrison, Wendy Tietz, C. Thomas, Greg Berberich, Catherine Seguin