Question:

The administrators of the City of Lyons have obtained approval from the City Council to centralize the computer facility as of January 1, 2025. An internal service fund is created to account for the activities of the computer facility. The City Council has approved a contribution of $25,000 from the General Fund for use as working capital and an advance from the Electric Utility Fund of $355,000 for the purchase of equipment and facilities. The $355,000 advance will be repaid by the internal service fund in 20 equal annual installments.

The following transactions relate to the establishment and operation of the Internal Service Fund.

Required:

Prepare the journal entries necessary in the Internal Service Fund to record the transactions and events described above. The chart of accounts presented below may be used as an aid. The closing account, “Excess of Billings to Departments over Costs,” is like the “Income Summary” account of a corporation.

Transcribed Image Text:

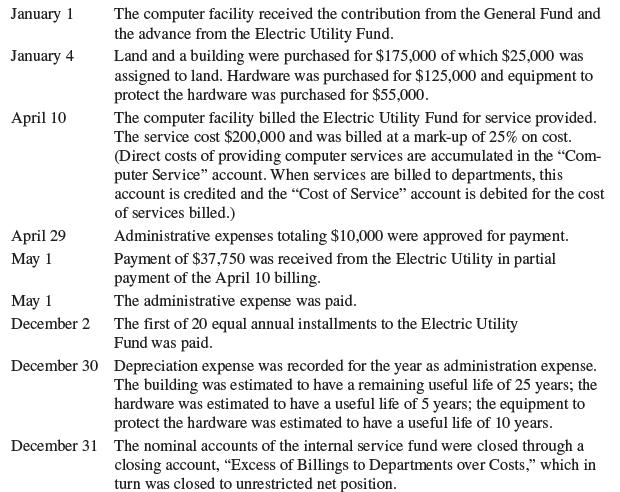

January 1

January 4

April 10

April 29

May 1

May 1

December 2

December 30

The computer facility received the contribution from the General Fund and

the advance from the Electric Utility Fund.

Land and a building were purchased for $175,000 of which $25,000 was

assigned to land. Hardware was purchased for $125,000 and equipment to

protect the hardware was purchased for $55,000.

The computer facility billed the Electric Utility Fund for service provided.

The service cost $200,000 and was billed at a mark-up of 25% on cost.

(Direct costs of providing computer services are accumulated in the "Com-

puter Service" account. When services are billed to departments, this

account is credited and the "Cost of Service" account is debited for the cost

of services billed.)

Administrative expenses totaling $10,000 were approved for payment.

Payment of $37,750 was received from the Electric Utility in partial

payment of the April 10 billing.

The administrative expense was paid.

The first of 20 equal annual installments to the Electric Utility

Fund was paid.

Depreciation expense was recorded for the year as administration expense.

The building was estimated to have a remaining useful life of 25 years; the

hardware was estimated to have a useful life of 5 years; the equipment to

protect the hardware was estimated to have a useful life of 10 years.

December 31 The nominal accounts of the internal service fund were closed through a

closing account, "Excess of Billings to Departments over Costs," which in

turn was closed to unrestricted net position.