Phoenix Press produces consumer magazines. The house and home division, which sells home-improvement and home-decorating magazines, has

Question:

Phoenix Press produces consumer magazines. The house and home division, which sells home-improvement and home-decorating magazines, has seen a 15% reduction in operating income over the past 15 months, primarily due to an economic recession and a depressed consumer housing market. The division’s Controller, Sophie Gellar, has been pressurized by the CFO to improve her division’s operating results by the end of the year. Gellar is considering the following options for improving the division’s performance by the end of the year:

a. Cancelling three of the division’s least profitable magazines, resulting in the layoff of 30 employees.

b. Selling the new printing equipment that was purchased in February and replacing it with discarded equipment from one of the company’s other divisions. The previously discarded equipment no longer meets current safety standards.

c. Recognizing unearned subscription revenue (cash received in advance for magazines that will be delivered in the future) as revenue when cash is received in the current month (just before the fiscal year-end), instead of depicting it as a liability.

d. Reducing liability and expenses related to employee pensions. This would increase the division’s operating income by 5%.

e. Recognizing advertising revenues that relate to February in December.

f. Delaying maintenance on production equipment until January, although it was originally scheduled for October.

Required

1. What are the motivations for Gellar to improve the division’s year-end operating earnings?

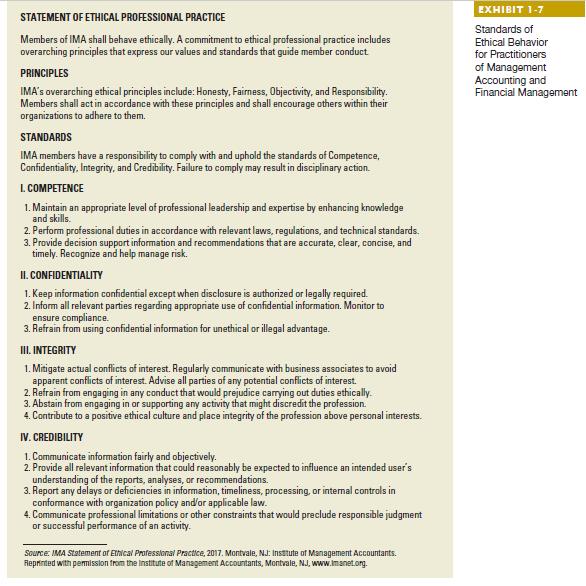

2. From the point of view of the “Standards of Ethical Behavior for Practitioners of Management Accounting and Financial Management,” Exhibit 1-7 (page 35), which of the preceding items (a–f) are acceptable? Which of the aforementioned items are unacceptable?

3. How should Gellar handle the pressure to improve performance?

Step by Step Answer:

Solution 1 They are i To reduce personnel costs ii To increase r...View the full answer

Horngrens Cost Accounting A Managerial Emphasis

ISBN: 9780135628478

17th Edition

Authors: Srikant M. Datar, Madhav V. Rajan