Your firm has been engaged to examine the financial statements of Almaden AG for the year 2022.

Question:

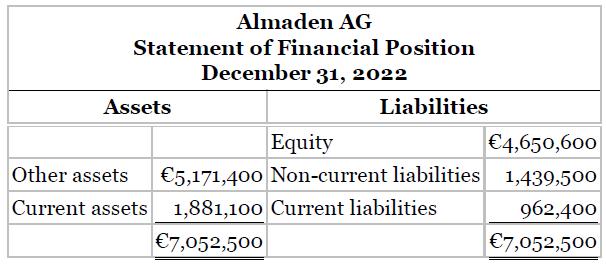

Your firm has been engaged to examine the financial statements of Almaden AG for the year 2022. The bookkeeper who maintains the financial records has prepared all the unaudited financial statements for the company since its organization on January 2, 2017. The client provides you with the following information.

Current assets include:

Cash (restricted in the amount of €300,000 for plant expansion) ..................................... € 571,000

Investments in land ...................................................................................................................... 185,000

Accounts receivable less allowance of €30,000 ....................................................................... 480,000

Inventories (weighted-average) ................................................................................................. 645,100

.................................................................................................................................................. € 1,881,100

Other assets include:

Prepaid expenses ....................................................................................................................... € 62,400

Plant and equipment less accumulated depreciation of €1,430,000 ................................ 4,130,000

Notes receivable (short-term) .................................................................................................... 162,300

Goodwill ......................................................................................................................................... 252,000

Land ............................................................................................................................................... 564,700

................................................................................................................................................... € 5,171,400

Current liabilities include:

Accounts payable ...................................................................................................................... € 510,000

Notes payable (due 2025) .......................................................................................................... 157,400

Estimated income taxes payable .............................................................................................. 145,000

Share premium—ordinary ......................................................................................................... 150,000

...................................................................................................................................................... € 962,400

Non-current liabilities include:

Unearned revenue ................................................................................................................... € 489,500

Dividends payable (cash) ........................................................................................................... 200,000

8% bonds payable (due May 1, 2027) ...................................................................................... 750,000

................................................................................................................................................. € 1,439,500

Equity includes:

Retained earnings ................................................................................................................ € 2,810,600

Share capital—ordinary, par value €10; authorized 200,000 shares, ................................. 184,000

shares issued ............................................................................................................................ 1,840,000

.................................................................................................................................................. € 4,650,600

The supplementary information below is also provided.

1. On May 1, 2022, the company issued at par €750,000 of bonds to finance plant expansion. The long-term bond agreement provided for the annual payment of interest every May 1. The existing plant was pledged as security for the loan.

2. The bookkeeper made the following mistakes. a. In 2020, the ending inventory was overstated by €183,000. The ending inventories for 2021 and 2022 were correctly computed.

b. In 2022, accrued wages in the amount of €225,000 were omitted from the statement of financial position, and these expenses were not charged on the income statement.

c. In 2022, a gain of €175,000 (net of tax) on the sale of certain plant assets was credited directly to retained earnings.

3. A major competitor has introduced a line of products that will compete directly with Almaden’s primary line, now being produced in a specially designed new plant. Because of manufacturing innovations, the competitor’s line will be of comparable quality but priced 50% below Almaden’s line. The competitor announced its new line on January 14, 2023. Almaden indicates that the company will meet the lower prices, which are high enough to cover variable manufacturing and selling expenses, but permit recovery of only a portion of fixed costs.

4. You learned on January 28, 2023, prior to completion of the audit, of heavy damage because of a recent fire in one of Almaden’s two plants; the loss will not be reimbursed by insurance. The newspapers described the event in detail.

Instructions

Analyze the preceding information to prepare a corrected statement of financial position for Almaden in accordance with IFRS. Prepare a description of any notes that might need to be prepared. The books are closed, and adjustments to income are to be made through retained earnings.

Step by Step Answer:

Almaden AG Statement of Financial Position As of December 31 2022 Assets Current Assets Cash restricted in the amount of 300000 for plant expansion 571000 Investments in land 185000 Accounts receivabl...View the full answer

Intermediate Accounting IFRS

ISBN: 9781119607519

4th Edition

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield