The long-term liabilities section of CPS Transportations December 31, 2023, balance sheet included the following: a. A

Question:

The long-term liabilities section of CPS Transportation’s December 31, 2023, balance sheet included the following:

a. A lease liability with 15 remaining lease payments of $10,000 each, due annually on January 1:

The incremental borrowing rate at the inception of the lease was 11% and the lessor’s implicit rate, which was known by CPS Transportation, was 10%.

b. A deferred income tax liability due to a single temporary difference. The only difference between CPS Transportation’s taxable income and pretax accounting income is depreciation on a machine acquired on January 1, 2023, for $500,000. The machine’s estimated useful life is five years, with no salvage value. Depreciation is computed using the straight-line method for financial reporting purposes and the MACRS method for tax purposes. Depreciation expense for tax and financial reporting purposes for 2024 through 2027 is as follows:

The enacted federal income tax rates are 20% for 2023 and 25% for 2024 through 2027. CPS had a deferred tax liability of $7,500 as of December 31, 2023. For the year ended December 31, 2024, CPS’s income before income taxes was $900,000. On July 1, 2024, CPS Transportation issued $800,000 of 9% bonds. The bonds mature in 20 years, and interest is payable each January 1 and July 1. The bonds were issued at a price to yield the investors 10%. CPS records interest at the effective interest rate.

Required:

1. Determine CPS Transportation’s income tax expense and net income for the year ended December 31, 2024.

2. Determine CPS Transportation’s interest expense for the year ended December 31, 2024.

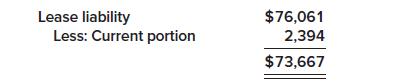

3. Prepare the long-term liabilities section of CPS Transportation’s December 31, 2024, balance sheet.

Step by Step Answer:

Calculation of 2024 Net Income Income before income tax 900 Income tax expense 225 Net income 6...View the full answer